KYC Verification for Digital Lenders in Kenya: Frequently Asked Questions and Quick Solutions

Key Highlights

- CBK now mandates that all licensed digital credit providers verify borrowers using a valid national ID and a live selfie with liveness detection before disbursing loans. Non-compliance carries fines up to KES 30 million under POCAMLA and daily penalties under CBK regulations.

- A robust KYC stack for Kenyan digital lenders combines IPRS-based ID verification, biometric selfie matching, tiered CDD/EDD workflows, and real-time PEP and sanctions screening, all optimised for mobile-first, low-bandwidth environments.

- Platforms like Signzy bundle ID verification, liveness checks, and AML screening into a single API designed for CBK-compliant digital lending workflows.

- 1. What is KYC, and what does it mean for a Kenyan digital lender?

- 2. What is eKYC, and how is it different from manual KYC?

- 3. What documents are required for KYC in Kenya?

- 4. What are the CBK's new ID and selfie verification rules for digital lenders?

- 5. What's the difference between CDD and EDD, and when does each apply to a Kenyan borrower?

- 6. How does KYC work end-to-end for a Kenyan digital lender?

- 7. How do I verify a Kenyan national ID through IPRS?

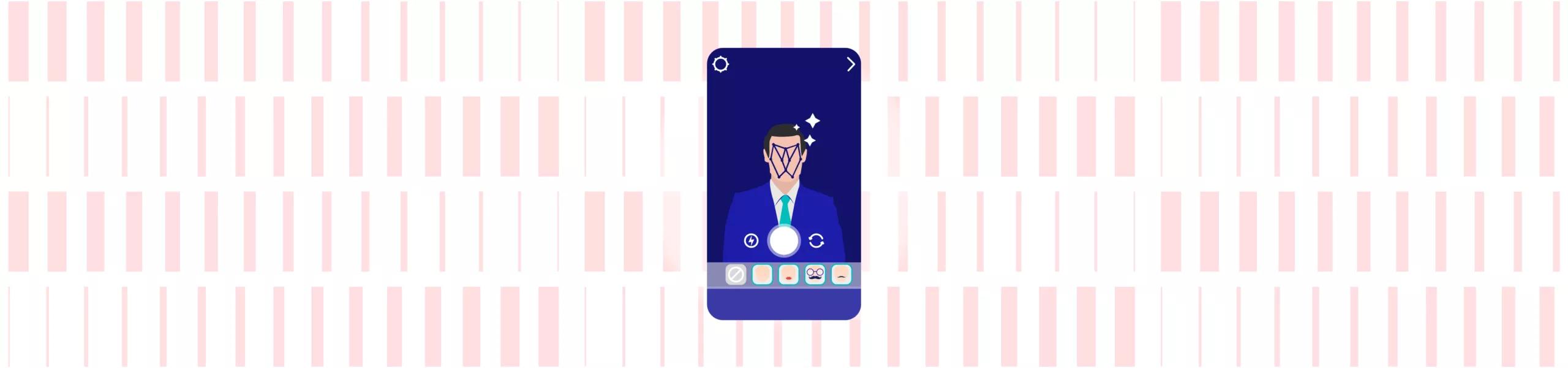

- 8. What is selfie verification, and how does liveness detection work?

- 9. Active vs passive liveness: which one should Kenyan lenders use?

- 10. How do I stop deepfake, SIM-swap and impersonation fraud at KYC?

- 11. How do I run PEP and sanctions screening on a Kenyan borrower?

- 12. How long should KYC take for a Kenyan loan applicant?

- 13. Why does ID verification fail, and how do I fix it?

- 14. How do I verify borrowers without a Kenyan national ID: refugee IDs, alien cards, minors?

- 15. What's the cost of KYC non-compliance under CBK and POCAMLA?

- 16. How do I integrate a KYC API into my loan origination flow?

- 17. What's the best KYC provider for CBK-licensed digital lenders in Kenya?

- How Signzy Helps Digital Lenders in Kenya

- FAQ

1. What is KYC, and what does it mean for a Kenyan digital lender?

Know Your Customer (KYC) is the regulatory process of verifying a borrower's identity and assessing their risk profile before establishing a business relationship. For Kenyan digital lenders, KYC is not optional. It is a legal obligation under multiple frameworks.

The Central Bank of Kenya (CBK) requires all licensed Digital Credit Providers (DCPs) to implement KYC as part of their licensing conditions under the CBK Act (Amendment) 2021 and the Digital Credit Providers Regulations, 2022. Separately, the Proceeds of Crime and Anti-Money Laundering Act (POCAMLA) classifies digital lenders as reporting institutions, which means they must conduct customer due diligence, monitor transactions, and report suspicious activity to the Financial Reporting Centre (FRC).

In practice, KYC for a Kenyan digital lender means:

- Collecting and verifying the borrower's identity using a reliable, independent source (typically the national ID checked against IPRS).

- Capturing a live selfie with liveness detection to confirm the person applying is the actual ID holder.

- Screening the borrower against sanctions, PEP, and adverse media lists.

- Maintaining records for at least 7 years and filing Suspicious Transaction Reports (STRs) when required.

The penalty environment is stacked: CBK can impose fines of up to KES 500,000 per violation plus KES 10,000 per day, POCAMLA penalties reach KES 30 million, and the Data Protection Act adds up to KES 5 million or 1% of annual turnover for mishandling borrower data.

2. What is eKYC, and how is it different from manual KYC?

Electronic KYC (eKYC) is the fully digital process of verifying a customer's identity remotely, using online channels instead of physical, paper-based checks. For a Kenyan digital lender, eKYC is the default onboarding method. It replaces branch visits, photocopied IDs, and manual form-filling with an in-app flow that takes seconds.

A typical eKYC flow for a Kenyan borrower:

- Borrower enters their national ID number in the lending app.

- The app captures photos of the front and back of the ID card.

- OCR extracts the name, ID number, and date of birth.

- The system cross-checks extracted data against IPRS or a trusted verification provider.

- The borrower takes a live selfie; the system runs liveness detection and face matching against the ID photo.

- AML/PEP screening runs in the background.

- If all checks pass, the borrower is verified and can proceed to loan application.

How it differs from manual KYC:

Manual KYC requires physical presence at a branch or agent location, paper forms, photocopied documents, and human review. Turnaround is hours to days. eKYC completes in minutes or seconds, scales to thousands of applications daily, runs 24/7, and produces a fully auditable digital trail.

CBK accepts eKYC for licensed digital credit providers, provided it is robust, risk-based, and compliant with AML/CFT obligations. The regulator is not pushing lenders back to branches. Instead, it is pushing them toward more rigorous digital verification, specifically the ID-plus-selfie standard now enforced across the DCP sector.

For mobile-first Kenyan borrowers, eKYC removes the friction of traveling to a branch, waiting in line, and producing physical documents. This is particularly important for rural borrowers, informal workers, and first-time credit users who may not have easy access to bank branches but do have a phone and a national ID.

3. What documents are required for KYC in Kenya?

The specific documents depend on the borrower's identity type and the lender's risk tier. Below is the standard document matrix for Kenyan digital lenders.

| Document Type | Who Needs It | Verification Method |

|---|---|---|

| Kenyan National ID (Maisha Card) | All Kenyan citizens aged 18+ | IPRS database check + OCR + face match |

| Kenyan Passport | Citizens without national ID; also accepted as primary ID | IPRS / immigration database check |

| Alien Card (Foreign National Certificate) | Foreign nationals resident in Kenya | Immigration database; accepted by CBK for account opening |

| Refugee Identity Card | Refugees registered with DRS/UNHCR | Recognised under 2025 SIM registration regulations; accepted by growing number of financial institutions |

| KRA PIN Certificate | Often required for credit products | KRA database verification |

| Selfie / Liveness Image | All borrowers (CBK mandate for DCPs) | Biometric face match + liveness detection |

For business borrowers (KYB), additional documents include the Certificate of Incorporation, CR12 form (company directors and shareholders), company KRA PIN, and beneficial ownership declarations, verified against the Business Registration Service (BRS).

The core requirement under CBK's framework is that the identity document must be verifiable against a "reliable, independent source." For most Kenyan borrowers, this means the national ID verified through IPRS. The live selfie is now effectively mandatory for all CBK-licensed digital lenders as an anti-fraud and compliance measure.

4. What are the CBK's new ID and selfie verification rules for digital lenders?

In 2025 and 2026, CBK significantly tightened borrower verification requirements for Digital Credit Providers. The core mandate: every licensed DCP must verify a borrower's identity using a valid national ID and a live selfie with liveness detection before disbursing any loan.

This is not a suggestion. It is enforced through the DCP licensing framework and AML/CFT supervisory expectations.

What the rules require

- Valid national ID verification: The borrower must provide a government-issued ID (national ID card, passport, or alien card) that the lender verifies against official databases.

- Live selfie with liveness check: The borrower must capture a real-time selfie through the lending app. The system must confirm the person is physically present (not a photo, video replay, or deepfake) and match the face to the ID photo.

- Risk-based due diligence: Lenders must classify borrowers by risk and apply enhanced checks where warranted.

- Data protection compliance: All biometric and identity data must be collected with clear purpose, stored securely, and used only for verification and fraud prevention, in line with the Data Protection Act, 2019.

Why CBK introduced these rules

The digital lending sector in Kenya grew rapidly with minimal oversight, leading to widespread identity fraud, loans taken using stolen IDs, and predatory practices by unlicensed apps. CBK's intervention aims to:

- Prevent fraudsters from using stolen ID numbers to take loans in other people's names.

- Ensure the person applying for a loan is the actual ID holder.

- Bring all digital lenders into a formal, auditable compliance regime.

- Protect consumers from identity theft and over-indebtedness.

Enforcement

As of early 2026, CBK had licensed 227 digital credit providers. Lenders operating without a licence face fines up to KES 5 million and up to 3 years' imprisonment. Licensed lenders that fail to implement adequate KYC face per-violation fines of KES 500,000 plus daily penalties of KES 10,000 for ongoing breaches. Major apps like Tala have publicly updated their KYC flows to comply with these rules, requiring ID upload and in-app selfie verification for all Kenyan users.

5. What's the difference between CDD and EDD, and when does each apply to a Kenyan borrower?

Customer Due Diligence (CDD) is the baseline KYC process applied to every borrower. Enhanced Due Diligence (EDD) is a deeper, more intensive process triggered by higher risk indicators. Both are required under POCAMLA and CBK guidelines.

| Aspect | CDD (Standard) | EDD (Enhanced) |

|---|---|---|

| When applied | Every new borrower at onboarding | High-risk borrowers or transactions |

| Identity verification | National ID + IPRS check + selfie/liveness | All CDD steps + additional document requests |

| Source of funds | Basic understanding of income/occupation | Detailed evidence: payslips, tax returns, bank statements, contracts |

| Approval level | Standard compliance workflow | Senior management approval required |

| Screening | Sanctions + basic PEP check | Deep PEP/RCA screening + adverse media + ongoing monitoring |

| Monitoring frequency | Periodic (e.g., annual review) | Enhanced: every 6-12 months or event-driven |

| Record detail | Standard KYC file | Expanded file with rationale for risk acceptance |

EDD triggers for Kenyan digital lenders

Under POCAMLA and CBK's risk-based framework, EDD must be applied when any of the following are present:

- Politically Exposed Persons (PEPs): Borrower is a current or former senior public official, or a close family member or business associate of one.

- High-risk jurisdictions: Borrower has ties to FATF grey-listed or sanctioned countries.

- Complex ownership structures: Business borrowers with opaque shareholding or shell company involvement.

- Unusual transaction patterns: Loan amounts inconsistent with stated income, rapid loan cycling, or structuring behaviour.

- Adverse media: Borrower appears in media reports linked to fraud, corruption, or financial crime.

- Non-resident borrowers: Foreign nationals or cross-border activity tied to the loan.

The key operational point: your loan origination system should automatically flag EDD triggers based on risk scoring, not rely on manual judgment. When EDD is triggered, disbursement should be conditional on completion of enhanced checks and, for PEPs, documented senior management approval.

6. How does KYC work end-to-end for a Kenyan digital lender?

Here is the standard KYC process flow for a CBK-licensed digital lender, from borrower onboarding to ongoing monitoring.

Step 1: Data capture

The borrower opens the lending app and enters basic personal information: full name, phone number, date of birth, and national ID number.

Step 2: ID verification

The app prompts the borrower to capture the front and back of their national ID. The system runs OCR to extract identity fields, checks document authenticity (layout, fonts, security features), and verifies the ID number and name against IPRS or a trusted verification provider.

Step 3: Selfie and liveness check

The borrower takes a live selfie. The system runs liveness detection (to confirm a real person is present, not a photo or deepfake) and biometric face matching against the ID photo. If scores meet the threshold, the biometric check passes.

Step 4: AML/PEP/sanctions screening

The borrower's name, date of birth, and ID number are screened in real time against sanctions lists (UN, OFAC, EU), PEP databases, and adverse media feeds. Clear results proceed; potential matches are escalated to compliance review.

Step 5: Risk classification

The system assigns a risk score combining KYC results, device signals (geolocation, device fingerprint, IP), and any available credit bureau data. Low/medium risk proceeds to standard approval. High risk triggers EDD.

Step 6: Credit decision

KYC outputs feed into the credit decision engine alongside credit scoring, repayment capacity analysis, and product eligibility rules. If KYC and credit checks pass, the loan is approved and disbursed (typically to M-Pesa).

Step 7: Ongoing monitoring

For the duration of the relationship, the lender re-screens the borrower when sanctions lists update, monitors transaction patterns for suspicious activity, and triggers re-KYC at defined intervals or when risk indicators change.

This entire flow, from opening the app to loan disbursement, should take under 5 minutes for a standard borrower. The best-performing lenders complete eKYC verification in under 30 seconds.

7. How do I verify a Kenyan national ID through IPRS?

The Integrated Population Registration System (IPRS) is Kenya's central government database that consolidates civil registration, national ID cards, passports, alien IDs, and linked records (KRA PIN, NHIF, NSSF). For digital lenders, IPRS is the authoritative source for verifying a borrower's identity.

What IPRS returns

When you query IPRS with a national ID number, the system returns:

- Full legal name (surname, first name, other name)

- Date of birth

- Gender

- Citizenship

- ID card serial number

- Photograph (base64 or bytes)

- Signature

- Place of birth and residence

- Linked records (KRA PIN, where accessible)

Integration options

Direct integration: Your institution applies to the National Registration Bureau for IPRS access. You receive VPN credentials, WSDL URLs for the SOAP-based web service, and web service credentials. Your backend connects via the VPN and calls methods like `GetDataByIdCard`. This requires significant infrastructure (VPN endpoint, SOAP client, security controls) and an annual subscription fee of approximately KES 1 million plus per-query charges.

Via an aggregator: Third-party providers maintain the IPRS VPN and SOAP integration and expose a modern REST API over HTTPS. You call a simple endpoint with the ID number and receive a JSON response with all IPRS fields. This is faster to implement, requires no VPN infrastructure, and is how most digital lenders integrate. Per-check costs are typically a few tens of shillings, with volume discounts.

Common failure reasons

- Invalid ID number: Typo or fabricated number; IPRS returns an error.

- Name mismatch: Borrower's entered name differs from IPRS record (nicknames, spelling variations, name changes after marriage).

- Incorrect serial number: The ID card serial number does not match the current card on file (replacement card issued).

- IPRS downtime: The system experiences intermittent outages, especially during peak periods. Implement retry logic with exponential backoff and a fallback to manual verification for extended outages.

- Stale records: Recent name changes or new ID issuances may not yet be reflected.

For non-Kenyan nationals, IPRS covers alien IDs but not foreign passports. Foreign borrowers using only a passport require alternative verification methods.

8. What is selfie verification, and how does liveness detection work?

Selfie verification is the process of capturing a borrower's face through the lending app camera and matching it biometrically against the photo on their identity document (typically extracted from the national ID via IPRS or OCR). It answers the question: "Is the person applying for this loan the same person on the ID?"

Liveness detection adds a critical layer: it confirms the face in front of the camera belongs to a real, physically present human, not a spoofing attempt. Without liveness detection, a fraudster could hold up a printed photo, play a video, wear a mask, or inject a deepfake feed to pass a simple selfie check.

How liveness detection works

Liveness systems analyse the selfie capture for biological and physical signals that distinguish a live person from an attack:

- Texture analysis: Real skin has micro-texture patterns (pores, fine wrinkles, colour variation) that printed photos and screens lack.

- Depth detection: A real 3D face reflects light differently from a flat surface. Some systems use multi-frame analysis or structured light to detect depth.

- Motion analysis: Natural micro-movements (blinking, subtle head shifts, blood flow under the skin) are difficult to replicate convincingly in a spoofed presentation.

- Environmental consistency: The system checks whether the lighting on the face is consistent with the environment, flagging anomalies that suggest a screen or injected feed.

For CBK-licensed digital lenders, the combination of selfie verification and liveness detection is now mandatory. It directly addresses the fraud vector of stolen-ID loans, where a fraudster uses someone else's ID number but cannot pass a biometric face match with liveness.

9. Active vs passive liveness: which one should Kenyan lenders use?

Active liveness requires the borrower to perform actions on command: blink, turn their head, smile, or follow an on-screen dot. The system captures video and checks whether the movements were performed naturally and in real time.

Passive liveness requires nothing beyond a normal selfie. The AI analyses a single image or short burst of frames in the background, checking for texture, depth, and environmental cues without any user interaction.

The case for passive-first in Kenya

For Kenyan digital lenders operating in a mobile-first, low-bandwidth environment, passive liveness should be the default for standard loan applications. Here is why:

- Lower friction, higher conversion: Research indicates that approximately 48% of borrowers abandon onboarding when flows are slow or cumbersome. Active liveness adds steps that confuse users, especially on low-end devices with laggy cameras.

- Bandwidth-friendly: Passive liveness works with a single image or very short capture, reducing data requirements. Active liveness requires streaming video, which fails more often on 3G networks.

- Device compatibility: Active liveness depends on reliable camera performance for motion tracking, which is inconsistent on budget Android phones common in Kenya.

When to escalate to active liveness

Use active liveness as a step-up control, triggered when:

- Passive liveness scores are borderline or inconclusive.

- The loan amount exceeds a defined risk threshold.

- Device signals are suspicious (emulator detected, virtual camera, same device linked to multiple identities).

- The borrower is flagged for EDD.

This tiered approach balances fraud prevention with user experience. Modern passive systems with integrated deepfake detection are strong enough for the majority of standard loan applications. Active liveness adds a second barrier for high-risk scenarios where extra assurance is needed.

10. How do I stop deepfake, SIM-swap and impersonation fraud at KYC?

Kenyan digital lenders face four primary fraud vectors at the KYC stage. Each requires a specific defence.

Deepfake and AI-generated identity fraud

Fraudsters use generative AI to create realistic fake ID images or inject deepfake selfie feeds to bypass verification. Across Africa, deepfake-driven biometric spoofing attempts surged approximately 15x year-on-year according to Smile ID's 2026 Digital Identity Fraud Report.

Defences: Deploy liveness detection with dedicated deepfake recognition models that inspect skin texture, lighting behaviour, compression artefacts, and frequency-domain anomalies. Do not rely on document OCR alone without real-time IPRS validation.

SIM-swap fraud

Fraudsters obtain a victim's ID and phone details, then bribe or social-engineer a telco agent to port the number to a new SIM. They then use the hijacked number to pass OTP-based KYC and take loans. According to a TransUnion H2 2025 report, 10% of surveyed Kenyans were targeted and fell victim to digital fraud between February and May 2025, with SIM-swap and mobile-money fraud among the leading vectors.

Defences: Integrate with Safaricom/Airtel SIM-change APIs. If the borrower's number had a SIM change within the last 24 to 48 hours, delay disbursement or require step-up verification. Reduce reliance on SMS OTP alone by using in-app cryptographic challenges or push notifications.

M-Pesa and mobile-money fraud

Fraudsters onboard using compromised or mule M-Pesa accounts, or use data harvested from agent transaction books (where ID numbers and phone numbers are logged) to power impersonation attacks. Agent collusion enables rapid cash-out after fraudulent disbursements.

Defences: Cross-check whether the M-Pesa registered name matches the KYC ID name. Flag accounts where the phone number ownership recently changed or was recently created. Monitor velocity patterns: first-time borrowers who instantly cash out the full loan via specific agents should trigger alerts.

Impersonation and social engineering

Fraudsters call or message victims pretending to be bank staff, CBK officers, or Safaricom representatives, extracting PINs, OTPs, and even selfie images "for verification" that are later reused for fraudulent KYC. The Global Anti-Scam Alliance (GASA) 2025 report found that 83% of Kenyans experienced at least one scam in the preceding 12 months.

Defences: Mandatory ID-plus-live-selfie verification (CBK rules) makes pure data-only impersonation harder. Layer device fingerprinting and behavioural analytics to detect when multiple IDs are used from the same device, or when device/IP patterns are inconsistent with the borrower's profile.

11. How do I run PEP and sanctions screening on a Kenyan borrower?

PEP and sanctions screening is a legal obligation under POCAMLA for all reporting institutions, including digital lenders. The Financial Reporting Centre (FRC) expects lenders to screen borrowers at onboarding and continuously as lists are updated.

Which lists to screen against

Mandatory (minimum):

- UN Security Council Consolidated List (binding on Kenya as a UN member)

- Kenya FRC Domestic Terrorism List (under POCAMLA and the Prevention of Terrorism Act)

Strongly recommended:

- OFAC SDN List (essential if you use USD corridors, have US investors, or process cross-border transactions)

- EU Consolidated Sanctions List (if exposed to EU banks or investors)

- PEP databases covering Kenyan domestic PEPs, foreign PEPs, and their relatives and close associates (RCAs)

- Adverse media feeds

How to implement screening

- At onboarding: Screen every borrower's full name, date of birth, and ID number against all configured lists before disbursing any loan.

- Ongoing re-screening: Automatically re-screen the full customer base daily or whenever lists update. PEP status changes (elections, appointments) must be caught promptly.

- Event-driven screening: Screen again before large or unusual transactions, when a borrower's risk score changes, or when new adverse media appears.

Most digital lenders use third-party screening APIs that aggregate global and African sanctions, PEP, and adverse media data into a single check. The API returns a match confidence score. Clear results proceed automatically. Potential matches are routed to a manual compliance review queue where an analyst compares identifiers (DOB, ID number, nationality) and documents the decision.

Handling matches

- Sanctions/terror list true positive: Do not onboard. Freeze relevant transactions. File an STR with the FRC immediately.

- PEP true positive: Not automatically prohibited, but trigger EDD. Obtain senior management approval, establish source of wealth and funds, and apply enhanced ongoing monitoring.

Maintain audit logs of every screening query, list version used, result, and reviewer decision. CBK and FRC inspections will look for evidence that screening is systematic and current, not sporadic.

12. How long should KYC take for a Kenyan loan applicant?

For a standard borrower using a Kenyan national ID, the entire eKYC process should take under 5 minutes from opening the app to completing verification. The best-performing digital lenders complete the core verification (ID check + selfie + liveness + AML screening) in under 30 seconds.

What drives speed

- Automated IPRS checks: Database lookups return results in 1 to 3 seconds when the system is responsive.

- On-device processing: Modern SDKs run OCR, image quality checks, and initial liveness analysis on the borrower's phone before uploading, reducing round-trip latency.

- Parallel processing: Run ID verification, AML screening, and device risk checks simultaneously rather than sequentially.

- Pre-filled data: For repeat borrowers, re-use previously verified data and only require a fresh selfie for re-authentication.

What causes delays

- IPRS downtime: The government database experiences intermittent slowdowns during peak periods. Build retry logic and a manual fallback queue.

- Poor network connectivity: On slow 3G connections, image uploads for ID and selfie take longer. Use compressed capture and resumable uploads.

- Manual review escalation: Borderline liveness scores, name mismatches, or AML flags that require human review add minutes to hours.

- Active liveness challenges: If the borrower must perform head turns or blinks, failed attempts and retries add friction.

The target for a Kenyan digital lender should be: 80%+ of standard applications fully verified in under 2 minutes, with manual review cases resolved within 24 hours.

13. Why does ID verification fail, and how do I fix it?

ID verification failures fall into four categories. Each has a specific remediation.

Data mismatch

The borrower's entered name or date of birth does not match the IPRS record. This is the most common failure. Causes include nicknames versus legal names, spelling variations, and mis-remembered dates of birth.

Fix: Implement fuzzy name matching with a configurable tolerance threshold. Allow partial matches (e.g., first name + ID number match) to proceed with a flag for review rather than an outright rejection. Display the IPRS-returned name to the borrower and ask them to confirm.

Document quality issues

The captured ID image is blurry, glare-affected, cropped, or too dark for OCR to extract fields reliably.

Fix: Use an SDK with real-time capture guidance: blur detection, glare warnings, framing overlay, and automatic recapture prompts. Reject low-quality captures before they reach the verification API.

Invalid or fake ID

The ID number does not exist in IPRS, or the document shows signs of forgery (incorrect layout, missing security features, manipulated text).

Fix: IPRS lookup catches non-existent IDs immediately. For forgery, use document authenticity checks that validate template layout, font consistency, MRZ (if applicable), and security feature presence. Flag discrepancies for manual review.

Infrastructure failures

IPRS is down or slow, the verification provider's API times out, or the borrower's network drops mid-flow.

Fix: Implement retry with exponential backoff for transient failures. Build a fallback queue where applications wait for IPRS to recover. For network drops, use resumable sessions so the borrower does not have to restart from scratch. Set clear SLAs with your verification provider and monitor uptime.

14. How do I verify borrowers without a Kenyan national ID: refugee IDs, alien cards, minors?

Not every borrower has a Kenyan national ID. A compliant lender needs alternative verification pathways.

Refugee Identity Cards

Kenya's Information and Communications (Registration of Telecommunications Service Subscribers) Regulations, 2025 explicitly recognise the Refugee Identity Card as a valid document for SIM registration. This establishes a legal precedent: the refugee ID is an officially recognised government document suitable for identity verification in regulated services.

For digital lenders, there is no CBK regulation that prohibits accepting refugee IDs. A lender can adopt refugee IDs as an accepted document, provided they have verification controls (document capture, liveness, and where possible, cross-referencing with DRS/UNHCR records). A growing number of KYC providers now support refugee ID verification.

Alien Cards (Foreign National Certificates)

The alien card is issued by the Department of Immigration to non-citizens legally resident in Kenya. CBK explicitly accepts alien cards for financial account opening (alongside national IDs and passports). Digital lenders can onboard foreign residents using a valid passport plus alien card, verified against immigration databases.

Minors (under 18)

Kenyan national IDs are issued at age 18. Minors lack the ID, and in most cases the KRA PIN, required for standard KYC. More fundamentally, contracts with minors have limited enforceability under Kenyan law.

In practice, digital credit to minors is extremely rare and generally not permitted by CBK-compliant lenders. Where a product involves a minor (e.g., education financing), the KYC model is:

- The parent or guardian is the primary customer, fully verified with their own national ID and KRA PIN.

- The minor is recorded as a beneficiary or dependent.

- No independent credit obligation is assigned to the minor.

---

15. What's the cost of KYC non-compliance under CBK and POCAMLA?

Non-compliance with KYC obligations exposes Kenyan digital lenders to a stacked penalty regime across three regulatory frameworks.

| Framework | Violation | Penalty |

|---|---|---|

| CBK DCP Regulations | Per KYC/AML violation | Up to KES 500,000 per violation + KES 10,000 per day the violation continues |

| CBK DCP Regulations | AML/CFT violation (legal person) | Up to KES 5,000,000 + KES 100,000 per day |

| CBK DCP Regulations | Operating without a licence | Up to KES 5,000,000 + up to 3 years' imprisonment |

| POCAMLA | Failure to implement KYC procedures | Up to KES 30,000,000 |

| POCAMLA | Failure to report STRs | Up to KES 30,000,000 + possible imprisonment |

| POCAMLA | Money laundering conviction | Fine + up to 14 years' imprisonment |

| Data Protection Act | Mishandling borrower data | Up to KES 5,000,000 or 1% of annual turnover (whichever is lower) |

Recent enforcement

The Office of the Data Protection Commissioner (ODPC) has been the most visibly active regulator against digital lenders. In 2023, Whitepath Company Limited received the maximum administrative fine of KES 5 million for mining borrowers' phone contacts and sending unsolicited messages to third parties. Mulla Pride Ltd (operating KeCredit and FairKash) was fined KES 2.975 million for unauthorized access to users' contacts and harassing repayment messages. In 2024, ODPC issued three penalty notices totalling KES 9.375 million against digital lenders and financial institutions for unlawful data sharing and failure to provide proper data collection notices.

On the CBK side, unlicensed digital lenders were ordered to cease operations after the licensing deadline, and CBK has made clear that repeated or serious regulatory violations can lead to licence suspension, revocation, and public gazettement of banned entities.

16. How do I integrate a KYC API into my loan origination flow?

Integrating KYC into your loan origination system (LOS) follows a standard architecture with Kenya-specific considerations.

Architecture overview

- Mobile app (front end): Embeds the KYC provider's SDK for document capture, selfie, and liveness.

- KYC orchestration service (backend): A single internal layer that calls verification APIs (ID check, biometrics, AML screening), normalises responses, and feeds results to the LOS.

- Loan origination system: Consumes KYC results as inputs to credit decisioning. Application states move through: `KYC_PENDING` → `KYC_PASSED` / `KYC_FAILED` / `KYC_MANUAL_REVIEW`.

- Audit/compliance layer: Stores all KYC requests, responses, images (or references), timestamps, and reviewer decisions.

Integration steps

Phase 1 (Days 1 to 3): Sandbox testing. Use the KYC provider's sandbox to test all verdict paths: pass, fail, manual review, timeout, and sanctions hit. Document response schemas and error codes.

Phase 2 (Days 3 to 7): Authentication and session management. Implement server-side API key management. Create an internal endpoint that generates short-lived client tokens for the mobile SDK. Never expose master API keys in mobile code.

Phase 3 (Days 5 to 10): Front-end SDK integration. Integrate document capture and liveness SDKs for Android and iOS. Test on low-end Android devices and slow 3G networks. Implement retry and resumable session logic.

Phase 4 (Days 8 to 15): Webhook handling. Expose secure webhook endpoints to receive asynchronous verification results. Verify HMAC signatures, implement idempotency keys, and normalise results into your internal schema.

Phase 5 (Days 12 to 18): Decision engine integration. Map KYC statuses to LOS business rules. Define thresholds for liveness scores, face match scores, and AML flags. Configure tiered workflows: micro-loans may require only ID database check, standard loans need full selfie and AML, high-value loans trigger EDD.

Phase 6 (Days 15 to 21): Logging and compliance. Implement immutable audit logs with timestamps, API response versions, and reviewer identities. Configure data retention per POCAMLA (minimum 7 years).

Best practices for Kenya

- Embed KYC early: Verify identity before running expensive credit bureau checks.

- Use tiered KYC: Match verification depth to loan size and risk. Do not run full EDD on every KES 500 micro-loan.

- Normalise behind an internal service: Avoid scattering vendor-specific code across your stack. This makes it easy to switch or multi-source providers.

- Optimise for latency: Target sub-2-second synchronous verification where possible. Run ID, AML, and device checks in parallel.

17. What's the best KYC provider for CBK-licensed digital lenders in Kenya?

The "best" provider depends on your scale, product mix, and technical maturity. But for CBK-licensed digital lenders, the evaluation should focus on four axes.

What to look for

1. Kenya-specific depth: Does the provider integrate directly with Kenyan government databases (IPRS, e-Citizen, BRS)? How many Kenyan ID types do they support? Providers with direct local integrations deliver faster, more accurate results than those relying on generic global OCR.

2. CBK compliance alignment: Does the provider support the ID-plus-selfie-plus-liveness standard CBK now mandates? Can they configure tiered KYC workflows (micro-loan tier vs. standard tier vs. EDD tier)? Do they provide audit-ready reports and case management for CBK inspections?

3. Mobile-first performance: How does the SDK perform on budget Android devices over 3G? What is the false reject rate for African faces? High false reject rates mean legitimate borrowers are blocked, directly hurting conversion and inclusion.

4. AML and screening breadth: Does the provider cover UN, OFAC, EU sanctions, Kenyan domestic terror lists, PEP databases, and adverse media? Can you configure risk thresholds and escalation workflows aligned with POCAMLA?

Pricing models

Most providers use per-check pricing (per ID verification, per liveness check, per AML screen), often with volume discounts and bundle options. Some offer subscription tiers with a fixed monthly volume plus overage. For digital lenders, the most cost-effective approach is tiered KYC: different check bundles for different loan sizes, so you are not paying for full EDD on every micro-loan.

When comparing cost, look at total cost of ownership, not just per-check price. A slightly more expensive provider with better fraud detection and fewer false positives can reduce fraud losses and manual review costs enough to be cheaper overall.

How Signzy Helps Digital Lenders in Kenya

Kenya's CBK-mandated ID and selfie verification rules demand a KYC stack that is fast, accurate on African faces, and built for mobile-first lending. Signzy's verification suite is designed for exactly this use case.

One-Touch KYC (OTKYC): Signzy's One Touch KYC bundles ID verification, liveness detection, face matching, and AML screening into a single API call. For a Kenyan borrower, this means one flow: scan the national ID, take a selfie, and receive a verified identity with sanctions clearance in seconds.

ID Verification: Supports Kenyan national IDs, passports, alien cards, and driving licences with OCR, document authenticity checks, and database cross-referencing. Signzy's document verification covers 14,000+ document types across 150+ countries.

Liveness Check: Signzy’s liveness checks detect photo replays, video injection, 3D masks, and deepfake attacks. Optimised for low-bandwidth environments and budget Android devices common among Kenyan borrowers.

AML and Transaction Monitoring: Real-time screening against global sanctions, PEP, and adverse media lists. AI-driven transaction monitoring with dynamic risk scoring identifies mule accounts and suspicious loan cycling patterns, helping lenders meet POCAMLA reporting obligations.

Tiered Compliance Workflows: Configure Tier 1 (ID + database check for micro-loans), Tier 2 (full selfie + liveness + AML for standard loans), and Tier 3 (EDD with manual review for high-value applications), aligning verification depth to loan risk and controlling per-borrower KYC cost.

FAQ

Do I need a CBK licence to offer digital loans in Kenya?

Can I use M-Pesa transaction data as a substitute for formal KYC?

How often do I need to re-verify a borrower's KYC?

Is biometric data (selfies) covered by the Data Protection Act?

What happens if IPRS is down and I cannot verify a borrower?

Are there specific KYC rules for borrowers in rural Kenya?

Saurin Parikh

Saurin is a Sales & Growth Leader at Signzy with deep expertise in digital onboarding, KYC/KYB, crypto compliance, and RegTech. With over a decade of professional experience across sales, strategy, and operations, he’s known for driving global expansions, building strategic partnerships, and leading cross-functional teams to scale secure, AI-powered fintech infrastructure.

Related Blogs

View all

CBK's New ID and Selfie Verification Rules: What Kenya's Digital Lenders Must Do Now

Online KYC Regulations for Digital Lenders in Kenya: Requirements, Process & Compliance Checklist

Selfie ID Verification API: How Can Your Business Stay Compliant and Safe?

AI-Generated Selfies: What are they and How Your Business can Counter them?

The best in business

The global API marketplace for KYC, KYB, & AML

Explore the end-to-end verification stack trusted by 1,000 businesses.

Get in touch