Online KYC Regulations for Digital Lenders in Kenya: Requirements, Process & Compliance Checklist

Key Highlights

- The Central Bank of Kenya (CBK) now requires every licensed digital credit provider to complete full KYC verification, including a national ID check, a live selfie, and a face match, before disbursing a single shilling.

- This guide breaks down every regulatory requirement into a practical compliance checklist you can hand to your team on Monday morning.

- Signzy's identity verification and liveness check APIs help Kenyan digital lenders meet these CBK requirements through a single, fast integration.

- What Are the Key KYC Regulations Governing Digital Lenders in Kenya?

- What Does the KYC Process Look Like for Kenyan Digital Lenders?

- The Complete KYC Compliance Checklist for Digital Lenders in Kenya

- What Are the Penalties for KYC Non-Compliance in Kenya?

- How Signzy Helps Digital Lenders Meet KYC Requirements in Kenya

- FAQ

Here's a number that should keep every compliance officer in Nairobi up at night: KES 500 million. That's how much Kenya lost to SIM-swap scams and stolen identities in 2025, according to industry estimates compiled from Safaricom investigations and Communications Authority data.

And SIM-swap is just one piece of the puzzle. Deepfake-driven biometric spoofing surged 15x year-over-year across Africa last year. Password theft and spyware attacks in Kenya jumped 83%. Nearly half of all cyber incidents in the country are identity-driven. If you're running a digital lending platform, your borrowers' identities are under constant attack.

The Central Bank of Kenya has noticed. As of December 2025, CBK has licensed 195 digital credit providers (DCPs), and hundreds of unlicensed operators have been ordered to shut down. In a landmark 2025 ruling, a Kenyan Small Claims Court threw out 139 cases filed by unlicensed lenders, deciding they can't use courts to recover loans they had no legal right to issue in the first place.

The bottom line? If you're a licensed digital lender in Kenya, a strong know your customer programme isn't just a compliance checkbox. It's what stands between you and crippling fines, licence revocation, or a courtroom humiliation. And if you're not yet licensed, the clock is ticking.

What Are the Key KYC Regulations Governing Digital Lenders in Kenya?

Three laws form the regulatory backbone of KYC verification for digital lenders in Kenya. If you're in compliance, product, or risk at a know your customer-regulated entity, you need to know all three inside out.

CBK Digital Credit Providers Regulations, 2022

This is the big one. Issued under the CBK (Amendment) Act, 2021, these regulations require every non-bank digital lender to get a CBK licence. To earn and keep that licence, your platform must demonstrate:

- Board-approved KYC, AML, data protection, and consumer protection policies.

- Systems that verify borrower identity before any loan is disbursed.

- A reasonable assessment of each borrower's ability to repay.

- Ongoing monitoring, record-keeping, and annual compliance reporting to CBK.

What does "verify borrower identity" actually mean in practice? CBK has made it crystal clear through supervisory directives: every one of the 195+ licensed DCPs must verify borrowers with a valid national ID and a live selfie before a loan goes out the door.

Proceeds of Crime and Anti-Money Laundering Act (POCAMLA), 2009

POCAMLA and its 2023 Regulations bring digital lenders under Kenya's AML framework. Think of it as the law that says "know who you're lending to, and flag anything suspicious." Key obligations include:

- Customer due diligence (CDD) using reliable, independent source documents.

- Enhanced due diligence (EDD) for higher-risk customers: politically exposed persons (PEPs), cross-border transactions, large loans.

- Suspicious transaction reporting (STR) to the Financial Reporting Centre (FRC) within 2-3 business days.

- Registration on the FRC goAML platform and an annual compliance report by 31 January.

- Record retention for at least seven years.

Kenya Data Protection Act, 2019

The Data Protection Act is the regulation that many digital lenders underestimate, until ODPC comes knocking. It governs how you collect, store, and process personal data, including the biometric data at the heart of your KYC process. The non-negotiables:

- A clear lawful basis for processing (legal obligation or contract performance, not blanket consent).

- Transparent privacy notices at sign-up.

- A Data Protection Impact Assessment (DPIA) before deploying biometric KYC at scale.

- Registration with the Office of the Data Protection Commissioner (ODPC).

- Strict data minimisation: scraping contact lists, SMS content, or other unrelated data will get you fined. Several digital lenders have already learned this the hard way.

| Regulation | Authority | Core KYC Requirement | Key Penalty |

|---|---|---|---|

| CBK DCP Regulations, 2022 | Central Bank of Kenya | ID + selfie verification before disbursement | KES 500,000/violation + KES 10,000/day |

| POCAMLA, 2009 (+ 2023 Regs) | FRC / CBK | Risk-based CDD/EDD, STR filing, sanctions screening | Up to KES 5,000,000 + 3 years imprisonment |

| Data Protection Act, 2019 | ODPC | DPIA for biometrics, lawful basis, data minimisation | Administrative fines, enforcement orders |

What Does the KYC Process Look Like for Kenyan Digital Lenders?

Let's walk through what actually happens when a borrower opens your app and applies for a loan. Every step in this know your customer workflow maps directly to a regulatory requirement.

- National ID capture. The borrower photographs their Kenyan national ID (or passport for non-citizens). Your system uses OCR to extract the name, ID number, date of birth, and other fields.

- Document verification. The extracted data gets cross-checked against government databases. Meanwhile, forgery detection scans for tampered, reprinted, or AI-generated documents.

- Selfie capture. The borrower takes a live selfie right there in your app. This is now mandatory under CBK directives for all licensed DCPs.

- Liveness check. Here's where you prove a real human is on the other side of the screen, not a printed photo, a video replay, or a deepfake. More on how this works below.

- Face match. The system compares the live selfie to the photo on the national ID. A match score confirms the person holding the phone is the legitimate ID holder.

- AML and sanctions screening. The borrower is checked against sanctions lists, PEP databases, and adverse media.

- Risk scoring and decisioning. Based on your KYC verification results, credit bureau data, and internal risk models, the system assigns a risk tier. High-risk borrowers trigger enhanced due diligence.

The whole flow, done right, takes seconds. Done wrong, it costs you your licence.

How Do Liveness Checks and Selfie Verification Actually Work?

This is the part that trips up a lot of product teams. A selfie by itself proves nothing. Someone could hold up a printed photo of the borrower, replay a video, or, increasingly, use a deepfake generated from a stolen ID photo.

A liveness check closes that gap. There are two approaches:

- Active liveness asks the user to do something: blink, smile, turn their head. The system verifies the response in real time.

- Passive liveness analyses the captured image silently, detecting presentation attacks using texture analysis and depth estimation. No user action needed, which means less friction and higher completion rates.

Both feed into a face match algorithm that compares the live selfie against the ID photo. Why does CBK insist on this combination? East Africa recorded the highest fraud rejection rate in Africa at 27% in 2024, while digital banks and microfinance institutions saw peak fraud rates of 35% and 30% respectively across all biometric and document verifications. Without a proper liveness check, you're essentially leaving your front door open.

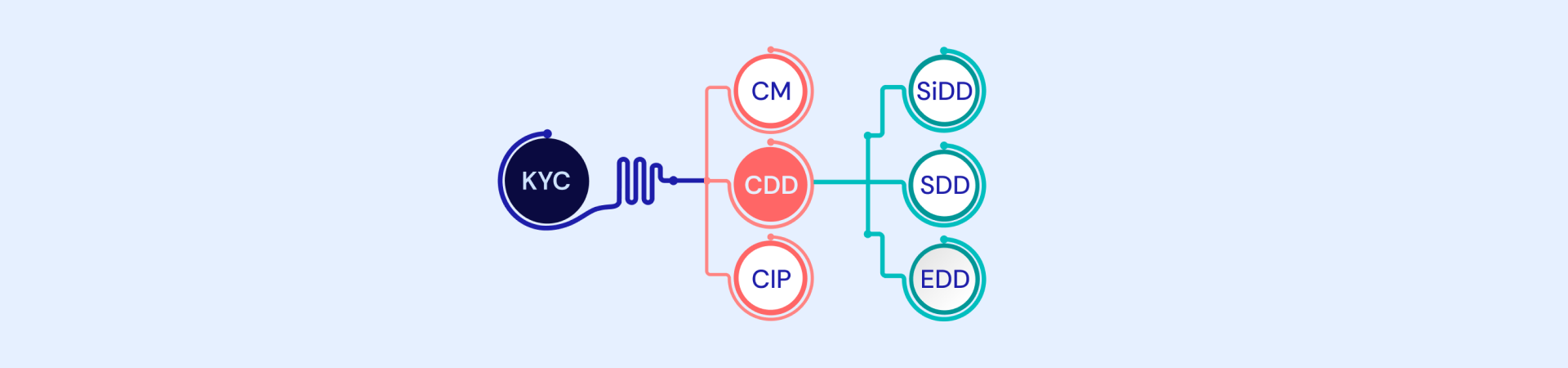

Tiered KYC for Different Risk Levels

Not every loan carries the same risk, and your KYC process shouldn't treat them all the same either. A compliant approach uses tiered verification:

- Tier 1 (low-risk, micro-loans): National ID verification, selfie with liveness check, face match, basic AML screening. This is the CBK-mandated baseline for every loan.

- Tier 2 (medium-risk, larger loans): Everything in Tier 1, plus income verification, credit bureau checks, and periodic KYC updates.

- Tier 3 (high-risk): Everything in Tier 2, plus enhanced due diligence, source-of-funds documentation, senior management sign-off, and increased monitoring.

The Complete KYC Compliance Checklist for Digital Lenders in Kenya

This is the section you'll want to bookmark (or print and pin to the wall). This KYC verification checklist pulls together every requirement from the CBK DCP Regulations, POCAMLA, and the Data Protection Act into one reference. Use it to audit your current KYC process, prep for a CBK inspection, or build a new programme from scratch.

1. Licensing and Registration

| # | Requirement | Regulatory Basis |

|---|---|---|

| 1.1 | Obtain a Digital Credit Provider licence from CBK | CBK DCP Regulations, 2022 |

| 1.2 | Register with the Financial Reporting Centre (FRC) on the goAML platform | POCAMLA, s.47A |

| 1.3 | Register with the Office of the Data Protection Commissioner (ODPC) as a data controller | Data Protection Act, 2019 |

| 1.4 | Ensure all directors and senior officers pass CBK's fit-and-proper assessment | CBK DCP Regulations, 2022 |

| 1.5 | Maintain transparent documentation of ownership structure and source of funds | CBK DCP Regulations, 2022 |

2. Customer Identification and Verification

| # | Requirement | Regulatory Basis |

|---|---|---|

| 2.1 | Capture and verify the borrower's national ID (or passport for non-citizens) before any loan disbursement | CBK DCP Regulations; POCAMLA CDD |

| 2.2 | Run OCR extraction on the ID document to capture name, ID number, date of birth, and other fields | CBK supervisory directives |

| 2.3 | Cross-check ID data against government databases or independent sources | POCAMLA; CBK KYC Guidelines |

| 2.4 | Perform document forgery and tamper detection on the ID image | CBK supervisory directives |

| 2.5 | Capture a live selfie of the borrower through your app or web channel | CBK mandatory selfie directive |

| 2.6 | Run a liveness check (active or passive) to confirm a physically present person, not a photo, video, mask, or deepfake | CBK mandatory liveness directive |

| 2.7 | Execute a face match between the live selfie and the photo on the national ID | CBK mandatory face match directive |

| 2.8 | Assess the borrower's ability to repay before disbursing the loan (income data, transaction patterns, CRB reports) | CBK Act (Amendment) 2021; DCP Regulations |

| 2.9 | Apply tiered KYC: enhanced checks for higher-value or higher-risk loans | POCAMLA risk-based CDD |

| 2.10 | Collect and verify business registration details, beneficial ownership, and director information for business borrowers (KYB) | POCAMLA; CBK Guidelines |

3. AML Screening and Transaction Monitoring

| # | Requirement | Regulatory Basis |

|---|---|---|

| 3.1 | Screen all borrowers against global and local sanctions lists (UN, OFAC, EU, Kenyan lists) at onboarding | POCAMLA; CBK AML Guidelines |

| 3.2 | Screen all borrowers against PEP databases at onboarding | POCAMLA; CBK AML Guidelines |

| 3.3 | Run adverse media checks at onboarding and periodically | POCAMLA; CBK AML Guidelines |

| 3.4 | Apply enhanced due diligence (EDD) for high-risk borrowers: PEPs, high-value loans, cross-border transactions, unusual patterns | POCAMLA; CBK Guidelines |

| 3.5 | Implement ongoing transaction monitoring with risk-based rules to detect suspicious activity | POCAMLA; CBK AML Guidelines |

| 3.6 | File suspicious transaction reports (STRs) with the FRC within 2-3 business days of detection | POCAMLA, s.44 |

| 3.7 | Re-screen existing borrowers against sanctions and PEP lists at regular intervals | POCAMLA; CBK AML Guidelines |

| 3.8 | Report borrower data to licensed Credit Reference Bureaus (CRBs) accurately and on time | CBK DCP Regulations |

4. Data Protection and Privacy

| # | Requirement | Regulatory Basis |

|---|---|---|

| 4.1 | Complete a Data Protection Impact Assessment (DPIA) before deploying biometric KYC (selfie, liveness, face match) at scale | Data Protection Act, 2019; ODPC Guidance |

| 4.2 | Document your lawful basis for each KYC data processing activity (prefer legal obligation or contract performance over consent) | DPA, s.30-33 |

| 4.3 | Provide a clear, accessible privacy notice at sign-up explaining what data is collected, why, retention periods, and data subject rights | DPA, s.25 |

| 4.4 | Collect only data that is necessary for KYC, AML, and credit assessment; do not scrape contact lists, SMS, or unrelated device data | DPA data minimisation principle |

| 4.5 | Encrypt biometric data (selfie images, liveness artefacts, face match templates) in transit and at rest | DPA, s.41; ODPC Guidance |

| 4.6 | Implement role-based access controls and least-privilege access for staff handling KYC data | DPA, s.41 |

| 4.7 | Establish processes to handle data subject rights requests: access, correction, erasure, and objection | DPA, s.26-30 |

| 4.8 | If KYC infrastructure or vendors are hosted outside Kenya, document cross-border transfer assessments and implement contractual safeguards | DPA, s.48-50 |

5. Governance and Reporting

| # | Requirement | Regulatory Basis |

|---|---|---|

| 5.1 | Maintain board-approved policies for KYC/CDD, AML/CFT, data protection, and consumer protection | CBK DCP Regulations |

| 5.2 | Appoint a designated AML Compliance Officer (MLRO equivalent) | POCAMLA; CBK Guidelines |

| 5.3 | Appoint a Data Protection Officer or equivalent responsible person | DPA; ODPC Guidance |

| 5.4 | Conduct regular staff training on KYC procedures, AML red flags, data protection, and fraud prevention | POCAMLA; CBK; DPA |

| 5.5 | Submit annual compliance returns to CBK confirming adherence to DCP Regulations | CBK DCP Regulations |

| 5.6 | Submit an annual AML compliance report to the FRC by 31 January each year | POCAMLA Regulations, 2023, Reg.44 |

| 5.7 | Notify CBK of any changes in significant shareholding, directors, or senior officers | CBK DCP Regulations |

6. Record-Keeping and Audit

| # | Requirement | Regulatory Basis |

|---|---|---|

| 6.1 | Retain all KYC documents (ID images, selfies, liveness logs, verification results) for at least seven years after the end of the relationship | POCAMLA; CBK DCP Regulations |

| 6.2 | Retain all transaction and loan records for at least seven years | POCAMLA; CBK DCP Regulations |

| 6.3 | Maintain a tamper-proof audit trail for all KYC decisions, including who/what system made each decision and when | CBK supervisory expectations; POCAMLA |

| 6.4 | Implement documented data retention schedules with automated deletion or anonymisation routines for data past its retention period | DPA data minimisation; ODPC Guidance |

| 6.5 | Ensure all records are easily retrievable for CBK, FRC, or ODPC inspections | CBK DCP Regulations; POCAMLA |

| 6.6 | Conduct periodic internal audits of the KYC, AML, and data protection programme | POCAMLA; CBK; DPA |

What Are the Penalties for KYC Non-Compliance in Kenya?

Let's talk consequences, because this is where it gets real.

| Violation | Penalty | Legal Basis |

|---|---|---|

| KYC/AML regulatory breach | Up to KES 500,000 per violation + KES 10,000/day while it continues | DCP Regulations 2022, Reg. 37 |

| Operating without a CBK licence | Up to 3 years imprisonment + KES 5,000,000 fine | CBK Amendment Act, 2021 |

| Unlicensed non-deposit credit provider | Up to KES 20 million or 3x the financial gain | Business Laws (Amendment) Act, 2024 |

| Persistent non-compliance | Licence revocation, director disqualification from any licensed financial institution | DCP Regulations 2022 |

| Data protection violations | Administrative fines, enforcement orders, criminal referral | Data Protection Act, 2019 |

To put that in perspective: a single KYC verification gap that sits unresolved for 30 days could rack up approximately KES 800,000 in fines before CBK even considers pulling your licence or barring your directors.

How Signzy Helps Digital Lenders Meet KYC Requirements in Kenya

Signzy provides a unified API platform that covers the full KYC verification workflow mandated by CBK:

- ID Verification: OCR extraction, database cross-checks, and forgery detection for Kenyan national IDs and passports.

- Selfie Verification and Liveness Check: Active and passive liveness detection with presentation attack defence against deepfakes and injection attacks. Results in seconds.

- Face Match: Biometric comparison between the live selfie and the ID photo.

- AML and Sanctions Screening: Real-time checks against sanctions lists, PEP databases, and adverse media at onboarding and ongoing.

- One Touch KYC (OTKYC): A single integration bundling ID verification, selfie capture, liveness check, face match, and AML screening into one flow.

Signzy's no-code journey builder lets compliance and product teams design branded KYC flows without heavy engineering, while maintaining a full audit trail for CBK inspections.

FAQ

What is KYC verification, and why is it required for digital lenders in Kenya?

What documents are needed for the KYC process at a Kenyan digital lender?

How does a liveness check differ from a simple selfie?

How long must digital lenders in Kenya retain KYC records?

What happens if a digital lender operates without a CBK licence?

Do Kenyan digital lenders need a Data Protection Impact Assessment for biometric KYC?

Saurin Parikh

Saurin is a Sales & Growth Leader at Signzy with deep expertise in digital onboarding, KYC/KYB, crypto compliance, and RegTech. With over a decade of professional experience across sales, strategy, and operations, he’s known for driving global expansions, building strategic partnerships, and leading cross-functional teams to scale secure, AI-powered fintech infrastructure.

Related Blogs

View all

KYC Verification for Digital Lenders in Kenya: Frequently Asked Questions and Quick Solutions

CBK's New ID and Selfie Verification Rules: What Kenya's Digital Lenders Must Do Now

![KYC Challenges: Common Issues + Solutions [2026 Guide]](https://cdn.sanity.io/images/blrzl70g/production/a54a1ddd2fec7fc298bd7152a176ce79ebdd74de-5642x1326.png)

KYC Challenges: Common Issues + Solutions [2026 Guide]

KYC Vs CDD – What is the difference

The best in business

The global API marketplace for KYC, KYB, & AML

Explore the end-to-end verification stack trusted by 1,000 businesses.

Get in touch