Welcome to our meticulously curated KYC/KYB category, a comprehensive repository dedicated entirely to the multifaceted dimensions of Know Your Customer (KYC) and Know Your Business (KYB). As we stride deeper into the digital era, the procedures around KYC/KYB have emerged as a fundamental pillar, ensuring secure and compliant operations within the financial landscape.

The articles housed in this category plunge into the complexities of KYC/KYB, discussing its inherent challenges, potential solutions, and its indispensable role in the realm of identity verification. Our articles traverse a wide array of topics, ranging from the application of artificial intelligence in customer due diligence processes to the impact of regulatory shifts on KYC methodologies. These writings cover a broad spectrum of subjects, offering relevance to businesses and professionals operating within the financial industry.

As a leading industry player in the domain of digital identity verification, Signzy stands at the helm of innovation in KYC/KYB. Our cutting-edge solutions are engineered to simplify KYC, making these procedures faster, more efficient, and notably secure.

Regardless of whether you’re a compliance officer diligently maintaining regulatory standards, a fintech entrepreneur navigating the challenging waters of the financial industry, or simply an individual interested in gaining a deeper understanding of the evolving world of KYC/KYB, our category offers a treasure trove of information and insights.

We invite you to join us on this journey of exploration as we dive into the future of KYC in the rapidly evolving digital age. Our articles aim to enlighten, inform, and provide a well-rounded perspective on the significant role that KYC processes play in today’s digital financial landscape. Welcome to a world where knowledge becomes power, and compliance becomes simplified.

Being the 6th biggest manufacturer of motor vehicles, the Indian Vehicular Industry is a behemoth with a $118 billion value estimation. The fact that this is expected to skyrocket to $300 billion by 2025 makes it an unleashed beast.

The current process of customer onboarding and underwriting involves multiple physical parameters with the in-person involvement of the client and the assigned agent. But with novel technologies and cutthroat competition on the rise, it is time insurers decide to upgrade their game. This article focuses on the current market of automobile verification, its challenges and the solution.

The Current Market for Vehicles in India

By 2021 India is expected to become the 3rd largest passenger vehicle market in the world. 2019 saw a 2.7% increase in production in the industry as compared to the previous financial year.

The industry is in a state of growth and it is the right time to take the initiative and utilise it. The current modes of processing can be upgraded with technology. This will help flourish in a cutthroat market like India.

The Primary Players In The Indian Vehicular Industry

There are numerous automobile companies competing in the Indian market. The top ones are:

With revenue of near Rs.300,000 Crore, Tata Motors Ltd. takes the lion’s share of the market. Tata currently has a 6.3% and 45.1% market share in passenger and commercial vehicles sectors, respectively.

Maruti Suzuki India Ltd dominates the passenger vehicles market with over 50% in market share. The Rs.83,281 crore revenue and a market cap of nearly Rs.200,000 crore is an impressive aspect.

Mahindra & Mahindra Ltd also holds a big chunk of the market with revenue heading over Rs53,000 crore and a market cap reaching more than Rs. 70,000 crore.

The two-wheeler giant Hero MotoCorp Ltd comes on top of its specific niche with 36% of the market share. The Rs 32,871 crore revenue and the 57,180 crore market cap is impressive for a primary two-wheeler manufacturer.

Other honourable mentions include Bajaj Auto Ltd, Ashok Leyland Ltd, TVS Motor Company Ltd, etc

What Are The Challenges Of The Industry

As is with most industries, the challenges in the vehicular industry also play a lot in parallel with the adoption of technology. Gone are the old days of physical processing of documentation and verification. With the advancing technology, the terrain is entirely changing.

Insurers must ensure that they can survive the peer competition. Technological services are available for verification and other related processes. But the coding required coupled with the complexity and unavailability of resources from a single portal is frustrating.

Why Is Signzy The Solution?

The solution to technological hurdles is not simply newer technology. It is the right newer technology. Signzy can provide this. With a quiver of products and resources, we can provide you with the state of the art technology while properly understanding your requirements.

Beginning with customer verification using OVDs such as driving license to the verification of the vehicle registration, Signzy’s plethora of APIs will suit you. APIs like DL verification API and Vehicle Registration APIs use government and other databases to cross verify the user’s credibility while maintaining the process seamless.

Since the Signzy portal is extremely customizable you can choose from the arsenal of APIs and other resources. This will help you avoid unnecessary roadblocks. The No-Code AI rule engine that we deploy makes integration and access easy and efficient. Signzy can make your verification processes seamless while maintaining the best security you can obtain.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Isn’t this the first question that comes to one’s mind when meeting a person for the first time? It is a natural question. In people’s conversations, a response is enough to close this question. But, it is different when dealing with institutions like Banks, Countries (immigration officers), and governments. Verifiable documentary evidence has to support the response. This is when an Identity Verification Service comes into play.

It doesn’t matter who you are. Documents must validate identity when dealing with institutions. A couple of years ago, a video went viral on the internet. It featured the tennis great Roger Federer. An usher at the Wimbledon center court did not allow Federer to pass without an ID document. For the record, Federer has won Wimbledon a record 8 times.

Businesses use identity verification services to ensure customers’ identity is true and accurate.

The identity verification service validates identity in the following ways

Using Government documents such as license, social security card, or passport.

Verify information from many sources – credit bureau or government databases.

Thus, identity verification service ensures successful KYC and Anti-Money Laundering (AML) compliance. It also reduces risks by fighting identity theft.

Your business may not have an identity verification service in place. It may already have one but is evaluating other options. Here are pointers to build a strong, successful, fintech, and sustainable identity verification process.

Compliance for an identity verification service

Law of the land still reigns supreme. Statutory and regulatory compliance is mandatory and no exceptions are advised for any identity verification service. On one end, there are KYC requirements that mandate access to identity, financial and personal information. On the other, there are privacy laws that regulate access to user-owned data. A paradox. It is this contradiction that identity verification service providers have to navigate.

KYC

In 2002, all financial institutions made KYC mandatory in the US. This was due to the USA Patriot Act of 2001, which came into being after the 9/11 tragedy. All KYC processes have to adhere to a customer identification program, called the CIP. The CIP also forms part of the institution’s anti-money laundering (AML) policy. Banks and Fintechs leverage KYC to assess customer profile and consequent risk.

Privacy Laws

On 25 May 2018, the European Union (EU) put a privacy law into effect – General Data Protection Regulation (GDPR). GDPR brought to the forefront the entire debate on data privacy. ‘User consent’ is the cornerstone of GDPR giving tremendous control to the user. The user now has the power to manage data – active and passive – that the user shares with other parties. The US too has many privacy laws, but none at a central federal level, unlike the EU’s GDPR. The Californian Consumer Privacy Act (CCPA) is often the most talked about and the most recent.

Be aware of legal requirements before zeroing in on an identity verification service. Adhere to all laws including KYC, Anti-Money Laundering (AML) regulations, and privacy. Violation of laws could invite major penalties or financial jeopardy.

Fraud Protection

The leading identity verification company Idology published the eighth “Annual Fraud Report 2021.” It says leaders call identity verification, the number one challenge in addressing fraud. It is not surprising. Covid-19 accelerated digital transformation initiatives across organizations. Identity verification was one of the top use cases. This at a time when incidents of fraud – financial, data breaches, identity thefts, and mobile fraud plays – are at historical highs.

Technology

Without technology, no identity verification service would be possible. The options are discussed below.

Optical Character Reader (OCR)

The world is still far away from complete digitalization. Most documents including those related to identity are still in paper form. OCR transmits the data from paper to electronic portals. OCR scans, recognizes, reads, and extracts written information from an identity document. It then verifies if the identity card submitted by the customer is legitimate or not. This allows customers to verify their identity through smartphones. OCR collects data from documents and encrypts it to follow regulations and reduce fraud.

Biometrics

Your smartphone asks for your fingerprint or your Face ID to unlock. Biological markers are impossible to replicate. These markers are best placed to customers into a password.

Biometrics goes beyond face id recognition. It could extend to DNA matching, iris scan, fingerprinting, voice, and even typing. Biometric identification captures and corresponds to people’s unique physical features/behaviors. Thus, it lends strong confidence to a business’s approach to identity verification.

Blockchain

Following the crypto-mania? The Bitcoin frenzy has overshadowed the technology that powers crypto – Blockchain. Blockchain is powering a broad range of applications from trade to music and even voting. Yes, voting in elections. Identity management is using blockchain too.

The beauty and strength of the blockchain are that it restores the right to privacy to the user. It is the user who decides what personal identity information to share. Thus, fintech balance the challenge of ensuring compliance while adhering to privacy laws.

Blockchain is a digital ledger of decentralized data. It lends itself well to solve the use case of identity verification. Consumers assign a digital identity or watermark for all transactions. They then decide which information to share. This makes the process speedy, convenient, and risk-free for both parties. Thus, leveraging blockchain technology can ensure that digital compliance is convenient yet secure. Digital identity verification solutions including Signzy are also utilizing blockchain to audit transactions.

Artificial intelligence (AI)

AI impacts identity verification in the following ways,

Replace the human in performing all mundane tasks e.g. physical verification of paper identity documents.

Quick real-time verification of captured information with a trusted database either public or private.

Fraud detection and prevention.

Artificial Intelligence (AI) fastens the identity verification process compared to humans. It also resolves the biometric issues related to aging, makeup, and facial hair. AI-driven platforms leverage artificial intelligence algorithms. They verify a selfie and a photo ID for a swift and accurate identity verification process. AI accepts many identity card formats and uses the selfie for more authentication. AI conducts real-time authentication with geolocation, IP address, and AML background check.

The technology stack supporting identity verification could start with one of the above. The stack could also be a combination. The decision would depend on the requirements and the business’ capability maturity. The choice of the technology stack should address compliance, fraud, and user experience.

Awesome User Experience (UX)

Identity verification is fraught with friction. In most cases, it is a frustrating experience for the users. Most users seem to have developed ‘acceptance’ to a poor user experience. Even the smallest convenience offered comes out as a great user experience. Balance awesome UX with the need for compliance and also preventing financial frauds.

Factors to consider

The approach to delivering a great UX could be guided by the following factors.

Avoid human intervention as much as possible

Ever imagined what would happen if the number of customers increased by 10 times? Wouldn’t it be tedious for your staff to keep up with the onboarding process? Thus, it would lead to bottlenecks causing the process to slow down. Higher the number of customers, slower the onboarding process. It’s an issue that can be exacerbated. Hiring more employees could solve this problem but wouldn’t be beneficial. Deploying automation will prevent this problem. It will avoid time-consuming processes, human errors, monotonous and repetitive tasks, improving productivity.

Need for speed and seamless experience

Customers hate waiting. The more you make them wait, the higher are the chances of you losing them. Sign-up abandonment is a reality, even if related to ‘mandatory’ services like banking. Unfamiliarity with the processes can be uncomfortable and frustrating for the customers. This causes poor user experience, resulting in abandonment and even churn.

Set user expectations

Identity verification is never a one-step process. It has to involve many steps. Setting user expectations at the outset can help manage user expectations better. Resetting user expectations at every step will help build a relationship. Thus, leading to eventual success.

Quick Wins

The single most important element in improving UX is simplicity. Achieve UX Simplicity by doing some of the following.

Autofill or automate the capture

One can’t imagine the joy one experiences on seeing a 15 field form partially auto-filled. A helpful dopamine shot. The availability of public and private databases of information can improve UX and cut errors of omission and commission.

Ask easy to remember information

Instead of asking the entire 9 number social security number (SSN) asking for the last 4 digits could catalyze action. Similarly, asking for information progressively (i.e. step by step) instead of all at once could reduce friction.

Fallback

Not every user who fails verification is a fraudster. Legitimate users may also be unable to verify ID because of genuine reasons (patchy internet, poor quality camera). So as not to impair UX, the system should provide for a fail-safe fallback including a manual process as the last option.

It is all coming together

Digitization will continue to grow. Institutions will juggle many factors in implementing identity verification solutions. Compliance will, without doubt, be the overriding factor in setting direction. E.g. The current COVID-19 pandemic is exerting another layer of verification for people’s movement. The continued growth in mobile users is making awesome user experience hygiene. UX should be as simple as ordering food on mobile, if not simpler. It is up to technology to do the tough balancing act between compliance and UX. It will be interesting to witness the future of digital identity verification. It will include compliance, mobile identities, cross-border imperatives, and artificial intelligence. Get ready for a machine soon asking you, “Who are you?”

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Know Your Customer, is essential in the online gaming realm to ensure the integrity, safety, and compliance of the platform. As the digital gaming industry expands, it’s imperative to verify the identity of players to prevent fraudulent activities, underage participation, and potential misuse for money laundering.

The global online gambling industry was worth more than $45 billion in 2017 and is predicted to rise to $94.4 billion by 2024. With such a stark rise in use and increasingly large sums of money moving through these entities, online gambling and gaming institutions are facing the same scrutiny to which other banks and other financial entities are subject. Prime targets for identity fraud, money laundering, and international financial crime, regulatory compliance is intensifying to ensure that online casinos and gambling institutions are taking serious measures to prevent such illicit activity.

However, as the demand for online gambling services increases, so does the stringency of regulatory compliance. Not only does this mean hiring a large compliance team to deal with the backlog, but online casinos are also now subject to higher costs and wait times for identity verification procedures. In this sense, manual KYC processing for casinos is a little outdated, offering a clunky solution that wastes time, squanders budgets, and is littered with errors.

The Backdrop Of Online Gaming In the USA

In the USA, online gambling establishments that have gross revenue of over $1 million are classed as non-bank financial institutions (NBFI). This means they must adhere to similar regulations as banks to help prevent fraud, financial crimes, and money laundering.

The Financial Crimes Enforcement Network (FinCEN) is responsible for monitoring the compliance of AML regulations under the Bank Secrecy Act (BSA). The BSE requires that financial institutions must help the government identify and prevent money laundering by identifying, flagging, and reporting certain suspicious activity and transactions. FinCEN has assigned this responsibility to the Internal Revenue Service (IRS) to ensure compliance measures are being met.

For relevant online casinos, AML measures include filing suspicious activity reports (SARs) for unusual transactions of over $5000, as well as reporting currency transactions of over $10,000. There are also extremely tight requirements for recordkeeping and receipt storage, as well as credit extensions over $10,000.

While all of these AML measures are a must, US online casinos are first required to accurately identify and verify customers using KYC processes. Failure to do so results in unbelievable fines.

In fact, the American Gaming Association (AMA) recently updated its policies. According to these new regulations, US users can not open an account without providing basic PII details: full legal name, address, and social security number. More importantly, however, no real money transactions can be undertaken without submitting an official government ID and proof of a permanent address.

The poignant point here is that AMA’s rules apply to the patron, not the casino as such. In this sense, a US citizen using an online casino in a different jurisdiction must still provide this information. If online gambling platforms don’t have measures in place for this, they are in danger of non-compliance.

Call For KYC In The Gaming Industry – How It Can Help?

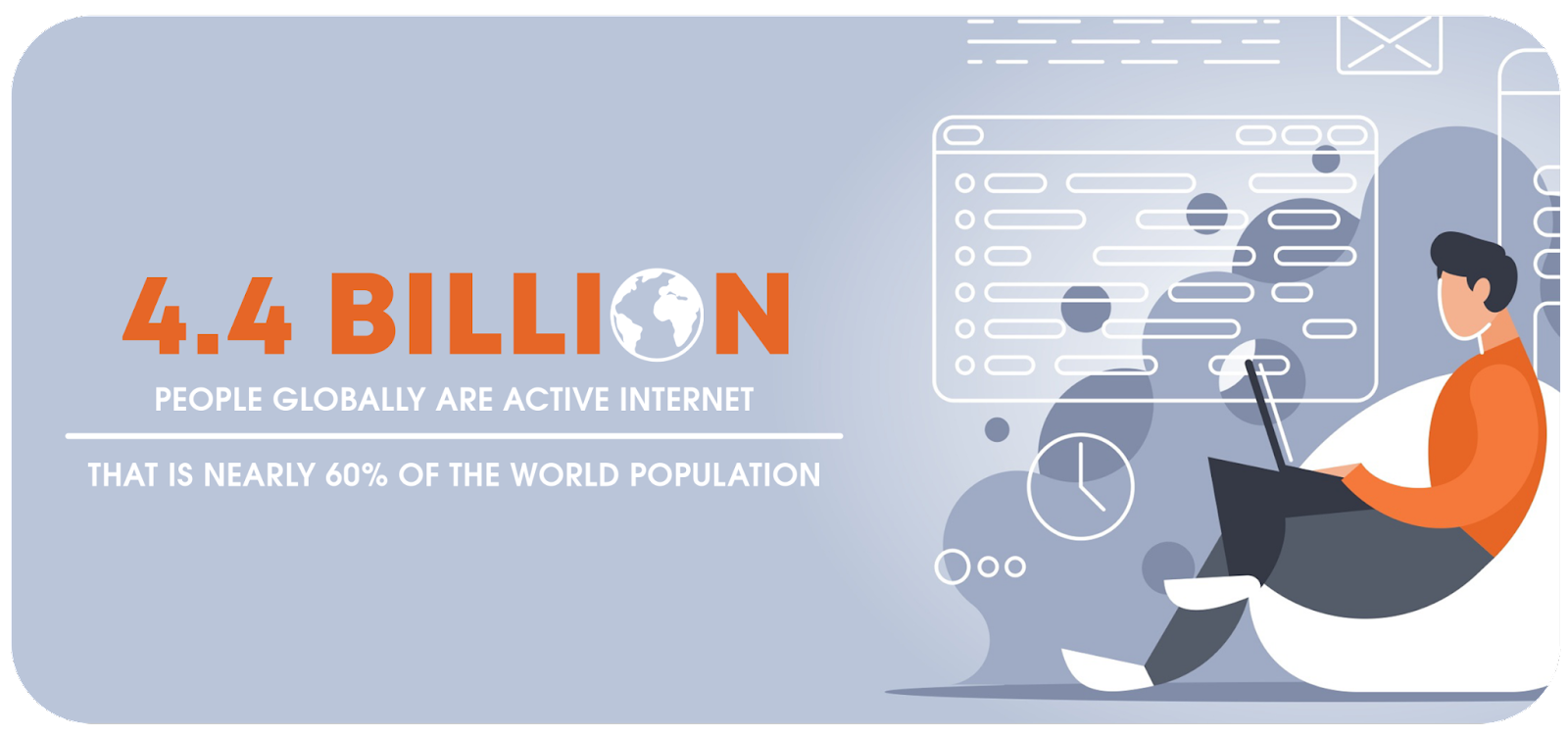

Almost 4.4 billion people globally are active internet users as of April 2019. This means that nearly 60% of the human population has the means to connect and interact with the online world around them. It’s no surprise that these combined factors have fueled the market for online gambling and gaming. In an already heavily regulated marketplace, this rapid growth is bringing Know Your Customer (KYC) and Anti-Money Laundering (AML) to the forefront of regulators’ agendas around the world.

With a wide range of options for users to gamble online, it makes sense that the companies that will come out on top are going to strike a balance between compliance and user experience. The question is, how can companies maintain compliance without sacrificing an incredible gaming experience for their users?

Why do online gambling and gaming companies need to be responsible for KYC?

Companies in the online gambling and gaming industries are legally obligated to verify user identity, age, location, and source of funds among other categories to protect their users and platform from bad actors and fraud.

One of the major reasons for this is the need to avoid money laundering and terrorist funding. If proper KYC is not performed on contestants and participants, the platform can be used to launder money and use it for assimilating funds for dangerous organizations. Many laws are created to prevent such practices and most gaming organizers and companies must abide to it.

Just as reputable companies prioritize trust when it comes to providing users with fair play and a secure environment, users must be able to trust that information being collected from them is being handled appropriately and safeguarded.

Companies looking to stay both in compliance and competitive are seeking advanced onboarding & identity verification solutions to…

Protect the company and users from bad actors and fraud

Continuously comply with the latest global regulations

Deliver a seamless, trustworthy, and user-friendly experience

KYC in The Gaming Industry – Mistakes That Could Be Avoided

Casinos deal in financial transactions, often on a very large scale. Online gambling platforms and casinos can turn over millions of dollars a day, making them a prime target for money laundering and financial crimes. Not only that, the lack of face-to-face interaction on internet gambling platforms makes it easier for fraudulent users to play on these sites without detection.

KYC and identity verification processes are designed to help reduce the risks of illicit activity by identifying customers and verifying that this identity is correct. In doing this, suspicious characters and potentially high-risk users can be flagged and monitored, or banned.

As in every industry, a risk-based approach is very important and necessary in the gaming industry. For an AML control program to achieve its purpose, it is very important to identify risks and take precautions against risks. As part of the risk-based approach, game operators must implement risk assessment by implementing AML controls to new customers throughout the customer engagement process. Know Your Customer and Customer Due Diligence procedures describe the controls that must be implemented during the customer onboarding process.

Currently, it’s predicted that 2-5% of the US’s GDP is laundered money, equating to between $800 billion and $2 trillion. Unfathomable sums of this nature have the power to shake the bedrock of the US economy.

While money laundering may seem to be a primary concern for banks and financial entities, studies show that casinos are ripe for money laundering. In 2014, Finnish gambling operators submitted over 9000 money laundering reports.

Studies are showing that criminal groups, known as dot.cons work together to ‘wash’ funds by deliberately losing games and claiming ‘clean’ prize money. A great example of this was The Corozzo Network, operating from 2005 to 2008. The network of 26 members ran illegal gambling and loan-sharking services through four online gambling sites, laundering more than $10 million.

More recently, CG Technology (trading as Cantor Gaming) was fined $22.5 million by various regulatory bodies in 2016 for poor AML provisions. The gambling company’s lack of AML procedures enabled 26 individuals, known as the ‘Jersey Boys’, to launder large sums of money through the platform with bad bets.

Further still, as technology advances, the schemes become more complex. Thanks to the introduction of virtual credit cards, prepaid mobile credit, and alternative payment gateways like PayPal, micro-laundering is now easier than ever and far less detectable.

By introducing strict KYC checks, casinos mitigate the risk of becoming vehicles for money laundering as high-risk individuals are flagged from the outset.

How Digital KYC Can Help The Online Gaming Industry

As we can see from above, KYC and AML (Anti Money Laundering) solutions can save business owners a lot of hassle. Digital KYC systems would have carried out comprehensive background checks identifying possible threats and allowing the owner to take action accordingly. The online gaming industry is a hotspot for money laundering although certain policies are governing the industry the chance is still there that it could be used for terrorist funding.

Signzy is an AI-powered RPA platform that provides digital onboarding solutions with our no-code AI model builder and our Fintech API Marketplace of over 200+ APIs. Our unique solution provides:

Secure System: A customer’s account information is secure because the entire process is online. Identity theft, fraud, loan scams, money laundering, the flow of black money, etc. are all minimized with RealKYC.

Efficient Communication: Effective information can be relayed in an efficient and timely manner. There is no need for constant back and forth. Most details are published automatically unlike manual KYC.

‘Free of Cost’ Process: RealKYC verification doesn’t charge any extra amount to the customer. A company or institution may need to pay automation costs of installing verification systems for the long run but the end-user gets a seamless, almost instant onboarding without hassle.

Faster processing: The RealKYC service is completely automated online. This means that KYC data can be transferred in real-time without the need for any manual intervention. The paper-based KYC process can take days up to weeks to get verified, but the eKYC process takes just a few minutes to verify and issue.

At Signzy, we have also introduced a new form of KYC verification called VideoKYC. This is a faster and more efficient form of KYC collection and verification. It conducts liveliness checks against the user as well as verifies the identification document against forgeries. The VideoKYC product has gained a lot of recognition and won several awards in recent months.

Advantages of using VideoKYC

Higher Application Accuracy

Plug and Play solution, swift Go-To-Market

Comprehensive Training Program

Competitive Advantage through customer delight

100% compliant with the latest RBI Mandate

Exponentially increase Scale of Operations

Reduced back office overheads (up to 70%)

Reduction in customer Drop-offs (up to 50%)

Platform Agnostic, support multiple communication channels

Conclusion

The online gaming industry is evolving rapidly around the world and expanding with each passing day. Gaming sites have improved tremendously in terms of user experience and now, they can make it more secure by enhancing the membership security protocols. Providing different gaming sites the ease of accurate digital ID verification will increase their revenue manifold. The introduction of digital KYC services has already been a huge success in financial and other sectors. Hopefully, its adoption in the near future might lead to more secure online gaming services in the US.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Health insurance policies are a vital instrument in the insurance industry. The Insurance Regulatory & Development Authority Of India (IRDAI), which acts as the regulatory body for all insurance companies in India, has allowed the use of paperless KYC collection, or e-KYC. This e-KYC will also be very useful in the current lockdown in the country. To enable this the government has allowed insurers to avail of the Aadhaar-based authentication services of the Unique Identification Authority of India

KYC Compliance Norms By IRDAI

IRDA has amended the Anti-Money Laundering (AML) guidelines and AML screening solutions which apply to general Insurers. This was done by circular no. IRDA/SDD/GDL/CIR/020/02/2013 on February 07, 2013. According to the guidelines. KYC documents (Proof of identity with photo, address proof) are compulsory for health insurance claims. This is highly applicable if the claim amount is Rs.1 Lakh and above.

Insurers need to verify the identity, address, and recent photograph (in the case of individual customers) as part of Know Your Customer (KYC) compliance norms. In this regard, the following documents are acceptable:

Recent photograph of payee

Proof of Photo Identity of payee

Proof of Residential Address of payee

The following documents are listed as valid Photo Identity Proof (Any One):

Passport

PAN Card

Voter’s Identity Card

Driving License

Aadhar Card

Letter from a recognized Public Authority. (As defined under Section 2 (h) of the RTI Act or Public Servant (as defined in section 2(c) of the ‘The Prevention of Corruption Act, 1988’)

Personal identification and certification of the employees of the insurer for the identity of the prospective policyholder.

Job card issued by NREGA duly signed by an officer of the State Government

The following documents are listed as valid Address Proof (Any One):

Telephone bill with respect to any kind of telephone connection. This can be mobile, landline, wireless, etc. This document should not be older than six months from the date of the insurance contract

Current Bank Passbook — details of permanent/present residential address (updated up to the previous month). Health insurance policies are a vital instrument in the insurance industry.

Updated bank account statement with details of permanent/present residential address

Letter from any recognized public authority

Electricity bill

Ration card

Aadhar Card

Valid lease agreement along with rent receipt which is within the last three months

Points to be NOTED:-

If the Insured person does not possess any of the above, then the following documents are acceptable:

Employer’s certificate as a proof of residence

Written confirmation of identification/proof of residence by the banks where the prospect is a customer

Medical Exam For Insurance

The Medical Exam is compulsory for many insurance companies, especially for volatile cases and cases with large claims value. It allows them to review your medical history and basic information that was used to make your insurance application.

All of the information is collected in the two stages of the medical exam. It is then combined with the statistical longevity data. The information on the insurance application is used to determine if you will be accepted for your insurance policy or not. It also determines what the annual premium will be.

The medical exam will usually include two parts:

A verbal questionnaire in which the medical professional will ask a series of health-related questions

Standard and basic sample collections: During the medical exam a sample of urine and blood may be required for submission. These tests can often be done in your home. You should be notified in advance by your insurance agent or broker which tests need to be conducted.

Duration Of The Medical Exam

The exam is approximately 20 minutes to thoroughly review your medical history verbally with the official. Then, it takes only a few minutes to collect the samples.

Need For Medical Exam By Insurance

There are three reasons health insurance companies administer medical exams:

To verify the authenticity of the information submitted to the company in the application

To review the full medical history of the applicant. The questions pertaining to the exam are designed for an in-depth analysis of your medical history and your family members.

To identify any underlying medical conditions. The applicant may be subject to medical conditions such as diabetes, inconsistencies in the blood work, or HIV. Sometimes the applicant may not be aware of the condition or may have chosen to not declare the same. The company will also verify drug or nicotine use. The information from the medical tests will be matched against the sample test results.

Need For Digitization in Health Insurance

Well, it’s nothing but the process of changing information into the digital format. With each passing year, digitization is becoming vital for the insurance industry. In 2005, people first started searching for digital insurance plans. Since then, digitization has consistently increased in strength in influencing the masses. Fast forward a decade and you can now buy digital policies online within a few minutes. You can find insurers everywhere, selling digital insurance online using social media prowess, and achieving resounding success.

The digital insurance market in the country is witnessing a compound annual growth rate of 25.36%. Digital media has played a crucial role in this spectacular growth and set the blueprint for digital insurance plans. Insurance companies embrace the digitization process with regards to proper digital norms as IRDA spearheads this empowering movement.

Despite filling the details on a website, this conventional method has the following drawbacks:

About 85% of the time and effort goes into manual form-filling, which is a huge pain point for customers and insurers alike.

The conventional method provides lesser room for fraud detection.

Human-errors can lead to catastrophic back-ops failures.

Increased turnaround time leads to increased time for processing claims, onboarding, etc.

Conducting a medical exam can also take time in terms of scheduling and verification.

What do the people gain from going digital for health insurance policies?

The conventional method can have the following disadvantages in terms of customer experience:

93% of customers get irritated by a lengthy & time-consuming onboarding process.

Lack of proper methods of ID verification leads to higher chances of fraud.

A bad customer experience during initiation leads to a broken onboarding journey.

Insurance policies like any other investment are prone to security risks which causes inconvenience to the insurance buyers. Apart from security, there are many other issues that will be resolved due to the Digitization of insurance policies. What is the solution? How is it related to Digitization?

Document portability: One of the major solutions offered by digitization is that the insured will get an e-copy of the documents related to the digital policies in question. Managing Documents has always been a hassle for policyholders. A majority of them end up losing premium receipts, policy cards, and other related documents. These documents may seem insignificant. However, if you plan on availing of tax deduction they can be a golden egg. If the insurance period ranges for more than 5 years, losing documents during such a long period of time may seem logical but is simply unacceptable. Here is where digital insurance comes into play. Since e-copies are stored in cloud-based data-servers; they can be preserved and acquired without putting in much effort. The documents are easily available on any digital device capable of reading and displaying the data. The database is managed by IRDAI approved Insurance repositories. They are

CDSL Insurance Repository Limited (CDSL IR)

Karvy Insurance Repository Limited

National Insurance-policy Repository by NSDL Database Management Limited

CAMS Insurance Repository Services Limited

Better customer service: When people visit the insurance providers for any clarification or data-related queries, they are given a date and are told to come on that day. When you ask them for a reason for this delay, they simply provide polite excuses. This solution is not acceptable for some customers who may require the documents on priority. This may be to file a return urgently or to claim the insurance money. With digitized management not only, the conservation of the data would be easy but providing the customers with the necessary information will be at the push of a button. With a properly formulated digitization, the process of handling customer queries like generating premium calendars, claims, and premium records, online payment of premiums, and tracking consumer requests will gain a faster pace leading to more satisfied customers.

No need to provide KYC for a new policy: When applying for any other type of insurance from the same company, the consumers are often asked for their KYC documents as identity proof. Here, Digitalization might be one of the most convenient solutions for consumers. With their KYC data stored in the company’s repository, all the company must do is overwrite the (Digital) application form with the data cached in their repository.

Monetary Efficiency: Not only do the providers who profit from digital insurance, but also the buyers experience ease in a transaction. Digital insurance can help the term insurance buyers save money on premiums with a 35–40% difference margin. How? When people buy term insurance, they usually buy it from an agent or a broker who adds brokerage or commission which is 30% of the insurance amount on the term insurance premiums. However, when you purchase term insurance online, you get insurance without any brokerage or commission added to the premium which saves you a margin of 30% easily.

Digital KYC For Fraud Prevention In Health Insurance

Fraud in the health insurance industry via impersonating a person is something where some people even go so far as to copy credit cards of another person and make payments using them. Fraudsters often use the medical insurance demographics of a person to gain healthcare benefits or purchase prescription drugs. Any of these situations can prove to be seriously harmful to the victim’s reputation.

Medical identity fraud has some extreme consequences on a person’s life. The financial shock can often be devastating for the insured. The emotional shock is of greater magnitude when a person gets their medical identity stolen. The medical institution itself has to overcome difficulties due to the type of fraud which it encounters. Medical identity theft is on the rise and a growing concern for both patients and healthcare providers. However, modern technology has revolutionized fraud prevention in healthcare.

The Healthcare industry is a booming sector in India and it is also replete with various challenges. Health insurance policies are designed with the intent of providing medical aid smoothly. It is equally vital to understand the health insurance details to gain optimum coverage.

However, the past decade has witnessed a rise in the fraudulent claims made by individuals. There is a constant need to revise the health insurance details, to avoid such deceitful claims. Both the insurance companies and policyholders must work together to tackle the problem.

Let us begin by first understanding the types of fraud in health insurance.

Different Types Of Health Insurance Frauds In India

Opportunity Fraud: This occurs when the policyholder provides inaccurate information while making a claim. One can hide a pre-existing condition or mislead the insurer to get the underwriting in their favor.

Deliberate Fraud: This involves the deliberate presentation of an accident or damage that is covered under the policy.

External Fraud: This is the fraud committed by policyholders, beneficiaries, medical service providers, or vendors against a company.

Internal Fraud: This is the fraud committed by agents, managers, or executives against a company. Even a policyholder can be at the cheating end of it.

Policyholder’s Fraud: It basically comprises the below-mentioned 3 types of frauds — claims, eligibility, and application.

Claim Fraud: Of the various other health insurance frauds in India, this is another one. Under this, the person can make an illegal claim to take advantage of the insurance coverage.

Eligibility Fraud: This is one of the many frauds in health insurance. It occurs when the person fills in incorrect information regarding the pre-existing condition or employment status.

Application Fraud: The concerned individual can enter wrong information to avail the extensive coverage.

Using AI for Fraud Prevention in Healthcare

Health insurance frauds in India can be checked by analyzing the fallacious behavior of frauds. Certain measures have been put in place to deal with health insurance frauds in India.

A strict screening process is being implemented by various insurance providers in India nowadays. Many insurance companies are leveraging technology to detect fraudulent behavior. In order to mitigate risks that threaten the healthcare industry, one must harness technical tools.

In today’s world, there are several third-party identity verification service providers. They offer digital KYC systems that use advanced AI and HI (Human Intelligence) to pick up attempts of fraud.

Online identity verification services authenticate individual users through document and facial verification techniques. This allows them to identify whether a person is using fake or stolen credentials and attempt to defraud the system.

KYC for a Better Customer Experience

Emerging technologies for online identity verification are critical because KYC adds friction to the onboarding process as customers go through the necessary identity verification steps. Long wait times are expensive for insurance companies and frustrating for customers who expect quick and easy interactions. In fact, research by Signicat found that more than 50 percent of retail banking customers in Europe abandoned their attempt to sign up for new financial services. The leading cause? The process simply took too long and was too onerous.

The challenge that every business faces, therefore, is how to balance KYC with the need for fast, efficient onboarding processes that deliver a positive customer experience.

Risk Management

It’s not enough to look at a customer’s risk profile only during the enhanced due diligence process of onboarding. Banks and other organizations must also look for signs of terrorist financing, suspicious activity, or other high-risk behaviors throughout the course of the business relationship.

In general, once a customer has been identified and verified, there is no requirement to re-verify their identity. The exception is when there is a trigger event, for example:

A product or service that you supply the customer changes

Suspicions are raised regarding previous demographic information collected and its authenticity.

Suspicions of money laundering are raised

By performing ongoing monitoring, businesses can implement a continuous risk assessment process that flags customers who may pose increased risks as circumstances change.

Digital KYC As A Means For Customer Onboarding In Health Insurance

With the latest norms for digitization, Signzy has developed two unique KYC products to suit all onboarding scenarios in the health insurance sector. RealKYC & VideoKYC have been developed in compliance with industry standards and offer you the following benefits:

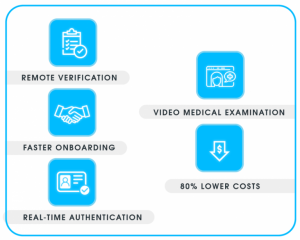

Remote Verification Of Medical Records: When purchasing a new health insurance claim, our digital KYC products ensure the authenticity of all submitted medical records.

Faster Onboarding Of New Insurers: Skip the long wait times for claim verification with RealKYC. Claims can be passed instantly as our patented AI helps reduce 90% of back-ops effort.

Real-Time Insurer Authentication: VideoKYC records the time stamp and audit trail for every application, ensuring all applications are authentic.

Online Medical Exam Through Video Conferencing: The insurers can directly connect with the medical examiner for the medical review which can be completed without hassle in a matter of minutes.

80% Lower Cost For Acquisition, resulting in easier and cost-effective onboarding

Future of digital insurance

Insurance, in most developed countries, is mandatory for every individual. Whereas, in India, policies like Mediclaim are availed only by people in urban areas. The insurance industry, however, is booming with success despite the facts. According to the reports from the BCG by the year 2020, a growth of 2,000 percent is predicted from its current state, while the turnover from the same range up to RS. 15,000 crore.

In a consumer trend analysis conducted by Google, there has been a significant 450 percent growth of searches related to life insurance and health insurance since 2008. On the other hand, the insurance industry itself has witnessed a 600 percent growth in the past five years. Experts believe, in the coming 2–3 years, 75 percent of insurance policy purchases all over the world will be done through digital channels.

The Government’s initiatives like Pradhan Mantri Suraksha Bima Yojana and Rashtriya Swasthya Bima Yojana encourage citizens to take insurance. Many governments in the country are in the early stages to digitize processes of obtaining and claiming insurance.

Digitization might be an elaborate process as most of the companies have employees who are not accustomed to the new digital procedures. On the other hand, it might need to be regulated with proper guidelines and rules to protect both the insurer and the insured against data misuse. One can say, Digitization will give a fair experience to each policyholder.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

The Life Insurance sector, historically reliant on paper-based processes and face-to-face interactions, is undergoing a transformative shift with the adoption of digital onboarding. This digital evolution not only streamlines the cumbersome enrollment procedures but also caters to the modern customer’s demand for quick, hassle-free experiences.

Life insurance policies play a crucial role in the insurance industry. The Insurance Regulatory & Development Authority Of India (IRDAI) is the regulatory body for all insurance companies in India. IRDAI has now allowed the use of paperless KYC collection or e-KYC. To enable this, the government has allowed insurers to avail the Aadhaar-based authentication services of the Unique Identification Authority of India (UIDAI)

Life Insurance Companies can use KYC For Fraud Prevention

Insurance fraud is a reality in this day and era. Many people who commit such frauds do so without realizing that their actions result in higher premium rates that have to be paid by other people. On average, insurance companies lose around $30 billion every year on account of fraud. The costs of these frauds are levied upon innocent, hard-working people. The necessity for fraud prevention systems in the industry is the need of the hour.

Moreover, the smaller cases are most harmful as they get ignored. After a while, they add up to become a cumbersome amount. Background checks are conducted in the insurance industry as they can single out money launderers, if not the fraudsters. Most people who engage in insurance fraud use fake or stolen identities to execute their schemes. As we proceed with the article, we will point out how KYC services providers can assist the insurance industry.

Frauds Mitigation Through KYC For Insurance

There are many types of frauds that happen with life insurance companies. However, some can be easily avoided by applying secure processes.

Fronting: The insurance policy is taken out using the details of another person to get favorable terms such as lower rates on premiums. Criminals or fraudsters usually use this process to carry out their scams. They use fake or stolen identities to identify themselves as someone else. Then they proceed to create fake documents to support their taken identity. KYC service providers can isolate such attempts and prevent them from happening.

Money Laundering: This is a global problem. Insurance companies too are a common target to launder money. The products offered by insurance companies are easy to target for fraudsters. This is because the processes that are associated with them make it easy for money laundering. Life insurance policies are extremely tempting to money launderers. This is because they allow for heavier premium deposits. Money Launderers take out such policies and deposit large amounts of money while canceling the policies after a while. KYC service providers conduct conclusive background checks. This helps prevent these types of frauds.

The KYC Screening Process

For a productive business, corporates require to deal with the right people with beneficial and favorable intent. Sectors that are particularly in the profession of handling money need to be careful. They must be sure that they are dealing with genuine entities. This is why the life insurance sector has to adhere to KYC norms mandated by their respective regulatory bodies.

As part of the Anti Money Laundering Act, KYC norms help in ensuring that the entity in question has an authentic identity. It is made sure that the source of money is not a shady one. The money would not be used for fostering any criminal activity either.

If we take the life insurance industry as an example, insurance companies deal with three entities-

the insured party

policy taker

agent.

All these entities need to be KYC screened.

Insured party — this is the entity on which the insurance policy is being taken making it imperative to be checked for authenticity. There have been instances when insurance policies have been taken on non-existent or fake identities or on persons who no longer exist. There also have been times when the policy is taken by tweaking a few pertinent details of an individual. The goal of KYC screening is to avoid such a situation.

Policy taker- the entity who is taking a policy should be eligible for taking such insurance. This is the rationale behind screening policy takers.

The insured party and the policy taker are screened with the same method. Their identity proofs are examined for authenticity and the specified address is examined by paying a site visit.

Agent- Insurance companies depend on agents to generate business. An agent is the one who markets the insurance products to individual customers. Agents also educate customers about various products and help them choose the most suitable one. Subsequently, they are also expected to provide all sorts of assistance in taking the policy, paying the premium, and receiving the insured amount when required. Given this significant role, insurance companies are extra cautious about their appointment of agents.

Drawback Of The Current KYC Process

Multiple insurance companies struggle to deliver digital experiences. This is because legacy applications are the most common obstacle for digital transformation. Onboarding a customer in lesser time with due diligence is a challenge.

The existing onboarding process for most insurance companies is similar to the following:

Customer lands on company website

Selects insurance type and plan

Fills-in Occupation, income details, and PAN details as (ID proof).

Life-cover details: pre-filled form

Basic Info: partially filled form

Customer Identity undergoes verification

Customer must enter Lifestyle-associated details

The customer fills the Nominee details

With digital KYC, the following areas can be addressed for a smoother customer experience::

Form filling is smooth

Liveliness check ensures more sanity

Telemedical video conference eliminates back and forth.

Digital Onboarding — Need For Digitization In Life Insurance

Industry analysts and large consulting firms claim onboarding is a top priority for digital transformation efforts across the insurance industry. After all, bad onboarding can increase customer attrition rates by between 25 and 40 percent, according to The Financial Brand.

Industry analyst firm Celent emphasized the need to focus transformation efforts on onboarding. In its November 2018 report, it also talks about industry trends for wealth management firms.

In a study by Bain & Company, customers who use digital channels tend to be loyal to their banks. Digital banking customers tend to own more products, and they transact and engage more with their banks. Mobile-first customers contribute to higher loyalty scores to their primary bank. This in comparison to the clients with low digital behavior. Globally, it is 50% higher approximately.

As noted by Argo executives at the InsureTech Connect conference in October 2018: “Customer acquisition is just the beginning. How you deliver value to customers — that’s the real benefit to them in this ecosystem. We’re trying to create a better experience for everyone we engage.” That means a better onboarding experience.

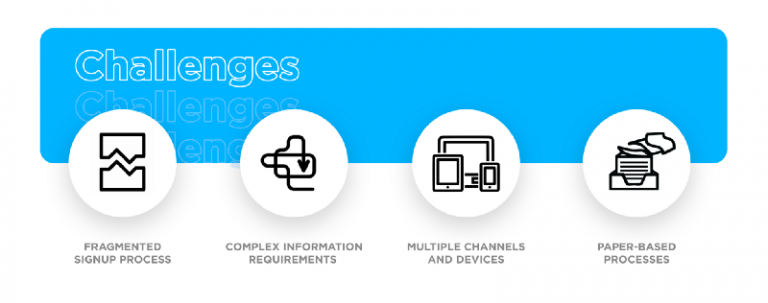

Major Challenges in The Life Insurance Onboarding Process

Fragmented signup process — There may be some customers who are unable to complete the signup process in just one session. Ideally, the onboarding process should track progress and let them stop. The process can later restart onboarding effortlessly, from where they left off.

Complex information requirements — Several industries have complicated data requirements and strict compliance regulations. Instances can be financial services, healthcare, and government. State or regional rules frequently oversee the information that needs to be gathered as well as the format. In general, customers have to sift through forms with irrelevant questions. This leads to a struggle to comprehend the exact requirement from them. This often results in high NIGO (not in good order) scores.

Multiple channels and devices — It is possible for customers to choose to onboard across multiple devices, or even via a call center. However, the experience is often inconsistent. Enterprises must provide clients with an integrated and seamless experience on each channel.

Paper-based processes — Many business processes require customers to complete and sign paper forms. They can either scan and fax or even worse, mail them back. No one enjoys this tedious and time-consuming effort, either externally or internally.

IRDAI Existing Guidelines For Life Insurance

Every insurer in the life insurance business must provide customized benefit illustrations to proposers or policyholders at the point of sale for all products. The exception can be to those issued under IRDAI (Micro Insurance) Regulations, 2015, Guidelines on Point of Sales (POS) — Life Insurance Products, 2016, and IRDAI (Insurance services by Common Service Centres) Regulations, 2019 as amended over time.

Such benefit illustration shall have to be signed by the prospective policyholder as well as the insurance agent. The signatories may also include the authorized person of an intermediary. Another alternative can be to include the insurer involved in the sales process, as the case may be, This should form part of the policy document.

Further, the benefit illustrations should be constructed as per the specific format prescribed by the IRDAI. The circular contains annexures specifying formats for these illustrations. These apply to different types of policies.

Need For Digital KYC — New Guidelines By IRDAI

Life insurance policy buyers will soon be able to complete KYC through a paperless process or e-KYC. This requires providing Aadhaar number as proof of identity to insurers, as per an IRDAI press release. This would make the Know Your Customer (KYC) process much easier for policy buyers.

This e-KYC will also be very useful in the current lockdown in the country. The government has allowed insurers to avail the Aadhaar-based authentication services of UIDAI. This can fulfill the KYC norms of policyholders.

The IRDAI press release, issued on April 24, 2020, mentions new KYC norms while availing insurance services. These norms will facilitate the general public to easily fulfill.

The release further states that the interested customers/policyholders/claimants may avail paperless KYC services in the coming days from the following insurance companies:

List Of Insurance Companies

Bajaj Allianz Life Insurance Company Limited

Bharti AXA Life Insurance Company Limited

Exide Life Insurance Company Limited

HDFC Life Insurance Company Limited

ICICI Prudential Life InsuranceCompany Limited

India First Life InsuranceCompany Limited

Max Life Insurance Company Limited

PNB Metlife India Insurance Company Limited

SBI Life Insurance Company Limited

Future Generali India Life Insurance Company Limited

Reliance Nippon Life Insurance Company Limited

Aegon Life Insurance Company Limited

Shriram Life InsuranceCompany Limited

Aditya Birla Sun Life Insurance Company Limited

Pramerica Life Insurance Company Limited

Kotak Mahindra Life Insurance Company Limited

Star Union Dai-ichi Life Insurance Company Limited

IDBI Federal Life Insurance Company Limited

Edelweiss Tokio Life Insurance Company Limited

Canara HSBC Oriental Bank of Commerce Life Insurance Company Limited

Kotak Mahindra General Insurance Company Limited

Future Generali India Insurance Company Limited

Manipal Cigna Health Insurance Company Limited

ACKO General Insurance Limited

Religare Health InsuranceCompany Limited

Royal Sundaram General InsuranceCompany Limited

SBI General InsuranceCompany Limited

HDFC Ergo General Insurance Company Limited

HDFC ERGO Health Insurance Limited (Formerly Apollo Munich Health Insurance Company Limited

KYC For Agent Assistance — How Digital KYC Helps

Agents are the fundamental constituents and the first step of the customer towards the onboarding journey. Insurance agents introduce customers to the various products on offer by a life insurance company. They also clear doubts and confusions of the customer and in many cases, collect the KYC for a new customer.

Given below are some highlights on why digital KYC can help insurance agents:

Client identification

The first step which involves identifying the correct name of the entity is a bigger challenge than most people would expect. A significant amount of time is wasted when front office staff or partners provide compliance with details, but of the wrong legal entity.

A common example is a deficiency of understanding in the front end around corporate structures. When a sales rep embarks on a new relationship with an entity, it’s easy for them to use the wrong name. It is very frequent for the holding company to not have the same name as the brand or branch with whom you are engaged in communication.

Initial risk assessment

This is a preliminary setup using customer-provided demographics to assign an initial risk rating, such as high, medium, or low. Such information can contain :

– director and shareholder details

– company incorporation documents

– a basic risk screen to identify major red flags, like sanctions.

Based on the top-level information provided on the client, it is easy to assess the level of risk they can inflict on your organization. However, not all customers will be high risk. With digital KYC, there is no need to dedicate time and resources to performing unnecessary due diligence steps which makes for an inefficient process.

Manual verification

Manual verification is a part of most traditional KYC processing workflows. They are multiple scenarios in which these aren’t the most efficient. Several agents have to go through several documents, make sure the information is correct and check for fraud. Humans aren’t anywhere close to being as fast as computers. Automating this process can mean a lot of time and money saved for the company, a higher rate of onboarding, and better employee satisfaction. Digital KYC can thus help remove the cost and time involved without any additional requirements from the agent side.

Authenticity of Agent

The primary channel through which insurance is sold in India is with the insurance agents. To increase the numbers for sales, agents may end up selling the wrong products to the clients. In such cases, agents do not provide complete information to the customers. This ultimately leads to customers who don’t get the best product. The consequence is a poor customer experience which is a loss for the industry. With Digital KYC, the insurance information can be identified. These cases can then be isolated to prevent further misuse by agents in the future.

Innovating Life Insurance with Digital Onboarding

For easier onboarding, Signzy has developed 2 unique Digital KYC solutions — RealKYC & VideoKYC.

With RealKYC, remote onboarding of new insurers is no longer a hassle. There are many benefits to RealKYC in the life insurance sector as follows:

Zero Paperwork: With RealKYC, customers can easily upload their KYC documents and IDs to the system. No need for making physical copies for manual submission.

Policy In Minutes: With RealKYC, customers no longer need to wait endlessly for the verification process to be completed. Get your life insurance policy active within minutes.

Easy Form Filling: Real-time data pre-population to eliminate manual form filling for submission of new claims.

VideoKYC has gained a lot of attention recently and has been the winner of multiple awards and accolades. With VideoKYC, you can get the following advantages:

Proof Of Life: With real-time in-person verification, insurance companies can easily establish ‘proof of life’ of the insurer from time to time.

Lesser chances of claims fraud: VideoKYC uses a host of Signzy’s proprietary APIs to verify all official documents and financial statements to mitigate potential claim frauds.

Conclusion

The fact that Digital KYC can be used for fraud prevention and to build trust is evident. Along with this, proper implementation will create a reliable and better onboarding process for the customers and the companies. This can be a boon for the Insurance Sector in India.

The operative word here is ‘proper’. Such an innovative idea demands excellent execution. That can be achieved by collaborating with credible associate companies and startups. If the insurance companies acknowledge this and process it, they will thrive in the booming Indian insurance sector.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok