Boomers, Gen X And Millennials- What Fintech Startups Get Right About Digital Onboarding?

By Signzian

- Introduction

- Some Banks Still Use Inefficient Traditional Methods To Onboard New Customers

- Why The Banks Aren’t Doing A Great Job at Digital Onboarding of Customers?

- Why Do Younger And Older Generations Respond Differently To Digitization?

- Fintech Startups Are Doing It Different… And Better

- What Can The Traditional Banks Adopt To Improve Their Services?

- Conclusion

Introduction

Onboarding a customer has always been a challenge to the Financial Industry. With the USA having less than 32 bank branches per 100,000 customers makes the entire procedure tedious for the customers. If creating an account online is not an option, they can spend days in the physical process of onboarding. Such bad customer experience and high customer drop-offs while onboarding is harmful to the institution. The solution is Digital Onboarding, which onboards customers remotely with the help of technology.

Digital onboarding is a relatively new method that has not been implemented to the fullest of its potential. But the worldwide availability of the internet has made it universally accessible if designed properly. Most financial institutions are already onboarding their customers digitally. But the processes in which they do are vastly different.

Compared to the traditional and established banks, the up and coming fintech startups are doing a better job at digital onboarding of customers. A closer look at this will provide traditional banks with new ideas to improve their systems. This is evident as Neo-banks like Ally and Chime went public, in the mid-2010s. Many more fintech startups are expected to follow suit.

💡 Related Blog:

Some Banks Still Use Inefficient Traditional Methods To Onboard New Customers

New customer onboarding is one of the most important issues retail banks face. When someone visits a website or walks into a branch to open a new account the bank doesn’t have a relationship with the customer, yet. It simply has a new account holder and actions need to be taken to move that relationship forward to become a long term profitable banking client.

Traditional methods trying to accomplish these goals are outdated, inefficient, and ineffective consisting primarily of paper brochures and phone calls from personal bankers.

Though. Most Financial institutions at this stage have upgraded their systems to digitize customer onboarding and engagement via a combination of apps and digital onboarding platforms.

Most of them though haven’t done this efficiently. Traditional banks form a major portion of this category while the neo-banks including fintech startups have done a far better job.

Usually, Traditional onboarding involves:

- Hardcopies of documents

- In-person verification

- 2–3 days required for onboarding

- An excessive requirement of space for storage

- Dreadful onboarding experience

This can be a long and excruciating process and the only reason customers put up with it was because of a lack of alternatives. In a way, almost all the existing financial services followed the same process.

This changed when NEO banks and other fintech came into being. Not only they gave an alternative from existing banks to the customers, but they were first to adopt the changing behaviour of the customers, which aligned towards everything digital, everything remote and everything private.

And this shows, from the rapid growth of NEO banks all around the world.

Why The Banks Aren’t Doing A Great Job at Digital Onboarding of Customers?

Most banks backed by regulators have slowly but steadily moved towards incorporating digital onboarding into their process.

Having said that, digital onboarding methods adopted by traditional banks have resolved some of these issues but they have not been efficient and leading to customers moving to NEO banks that offer a much easier onboarding and management. Some of the issues with traditional banks digital onboarding processes are:

- Confusing interface-. Customers find it difficult to navigate the facilities provided online.

- Extra charges and fees for digital access- many banks charge their customers for an online presence which can be provided for free.

- Onboarding time can further be reduced as the process is confusing and results in wasted time.

- Customer experience is poor- The applications and software used are not optimised to make the journey easy for the customers.

- The targeted customer base is mostly from Baby Boomers and Generation X who are mostly unfamiliar with digital technology.

Some traditional banks have had the foresight and done the necessary to cope with advancing times. A good example is that of Bank of America. The Bank focused on digitization since 2015 which yielded excellent results. The company onboarded more than 20 million users between 2017 and 2020, the majority of whom were onboarded digitally. Unfortunately, barring a few titans like JPMorgan Chase & Co. and Citibank, most of the traditional banks are behind in adapting to digitization.

Why Do Younger And Older Generations Respond Differently To Digitization?

Hard data available indicates only 8% of US customers consider an online bank as their primary bank. Prima facie this might seem unimportant. But the numbers almost double to 14% when it comes to customers with two accounts. The share rises to a staggering 17% with Americans who have 3 accounts. These numbers became 2 digits as late as the mid-2010s.

The reason attributed to this is the level of comfort and convenience of online banking offers. More than 56% of Americans acknowledged this. Hence, this indicates that there is a market for online banking, but better onboarding procedures are required.

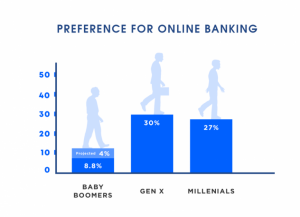

While there is a general consensus that younger generations usually prefer completely online procedures, even the older ones are warming up to the concept. 30% of Gen X and 27% of Millenials have an online-only account while 8.8% of Baby Boomers also embraced the online platforms according to Finder. They also reported that more than 4% of Boomers planned to open an online account. If they are keen on accepting online banking as a primary option, then digital onboarding is simply the first step in it.

Fintech Startups Are Doing It Different… And Better

Fintech Startups acknowledge the customers’ needs to a great extent plus being the upstarts in an industry dominated by behemoths they had to find ways to optimize costs and play on their strengths.

That’s one of the major reasons why they optimized user experience over everything else (since everything else was usually well defined by the regulators) leading to their digital onboarding systems to cater to even the most unfamiliar users. What might take days at traditional banks could be done within hours or even minutes through the new banks.

They know that even though boomers constitute the majority of the clientele and funds right now, in the long run, they will need loyal millennials on their side. Thus they cater to the need of the new. Most of their products and services are focused on Millennial and Gen X but yet are easy for the older clients to handle. Their digital onboarding procedures are designed to not tire the customer. Their primary aim is to get customers on board.

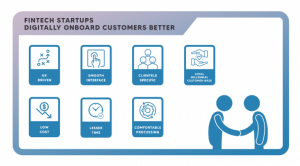

In brief, some of the important steps taken by fintech startups to better their customers’ digital onboarding journeys are:

- User Experience driven process

- Easy interface for onboarding

- No or Low Cost of Onboarding

- Reduced Time for Onboarding with Automation

- Defining Clientele for Long Term Benefits

- Comfortable Onboarding Process

- Developing Loyal Millennial Customer-base

What Can The Traditional Banks Adopt To Improve Their Services?

In theory, the Traditional Banks should acknowledge and adopt the right approaches Fintech Startups use to improve their customer onboarding. But in closer observation, we will see that all that the new banks are doing will not benefit the Traditional Titans. The methods require scrutiny before implementation.

A good example is how different the primary clientele is for both groups in terms of age. A ditto approach of focus on newer generations will distance the traditional bank’s existing customers. But a good plan to secure future customers must also be implemented. Hence, Traditional Banks have the task of retaining their existing customer base while expanding it into newer generations.

Since they have enough funds to back them, they should emphasize on better research and outsourcing to international fintech startups. This will improve their digital onboarding processes. These companies would exhibit no competition in the US market. A collaboration would enable the traditional banks to understand and access the new ideas and models they bring.

Along with this, banks need to improve the overall experience of the customer. This results in:

- Better User Experience

- Lower Cost of Onboarding

- Faster Processing

- And all the aforementioned benefits of digital onboarding

Conclusion

As the USA is moving towards a more advanced future where remote access is preferred and time is of the essence, onboardings will be digitized. The entities in the financial sector are aware of this which has rendered them to upgrade their current systems. This is regardless of them being traditional giants in banking or the up and coming startups in financial technology.

Amid such cutthroat competition, banks must find ways to expand their customer base. As it is with most cases, the trouble is always getting started. An easier and more convenient experience of digital onboarding is what the customer seeks to begin his journey with a new bank. If traditional banks can cater to this with attractive options, they will flourish in the coming decades.

If the banks acknowledge the needs of the customer and empathize with their struggles, they can provide far better services. The banks being the spine of the financial sector need to make the changes. These changes will cause a ripple effect in the sector, advancing it towards a modern world.

About Signzy

Signzy is a market-leading platform redefining the speed, accuracy, and experience of how financial institutions are onboarding customers and businesses – using the digital medium. The company’s award-winning no-code GO platform delivers seamless, end-to-end, and multi-channel onboarding journeys while offering customizable workflows. In addition, it gives these players access to an aggregated marketplace of 240+ bespoke APIs that can be easily added to any workflow with simple widgets.

Signzy is enabling ten million+ end customer and business onboarding every month at a success rate of 99% while reducing the speed to market from 6 months to 3-4 weeks. It works with over 240+ FIs globally, including the 4 largest banks in India, a Top 3 acquiring Bank in the US, and has a robust global partnership with Mastercard and Microsoft. The company’s product team is based out of Bengaluru and has a strong presence in Mumbai, New York, and Dubai.

Visit www.signzy.com for more information about us.

You can reach out to our team at reachout@signzy.com

Written By:

Signzy

Written by an insightful Signzian intent on learning and sharing knowledge.

Signzian

The best in business

The global API marketplace for KYC, KYB, & AML

Explore the end-to-end verification stack trusted by 1,000 businesses.

Get in touch