KYC in Algeria: Key Regulations and Compliance Requirements

May 16, 2025

4 minutes read

- KYC (Know Your Customer) in Algeria refers to the process of verifying the identity of customers to prevent money laundering and terrorist financing, following the country’s strict regulatory guidelines

- Businesses must verify identity using official documents like the Algerian National ID, passport, or driver’s license, along with proof of address, such as utility bills or bank statements.

- Businesses can stay compliant by integrating automated KYC solutions, conducting regular checks, and reporting suspicious activities to the CTRF as required by Algerian law.

If you’re eyeing the North African market for financial services or banking expansion, you’ve probably mapped out your regulatory research and tried to know more about Algeria’s KYC requirements.

It was a bit of the same journey for me. And while gathering information, I noticed there aren’t many comprehensive resources available in English, so I thought it would be helpful to compile what I’ve learned.

Based on my research, I can say Algeria has some fascinating specifics when it comes to customer verification – different from neighboring Morocco and Tunisia in several key ways.

This isn’t meant to be the final word on Algerian KYC, but hopefully it gives you a good starting point if you’re looking to understand how identity verification works in this important market. So, here we come.

Let’s dive right in. Takes 9 minutes.

KYC in Algeria, Quick Overviewrs

KYC in Algeria is based on the law set out in 2005 and updated in 2015: Loi n°05-01 (Law 05-01). The government’s focus is on preventing money laundering and terrorist financing. Businesses in Algeria need to verify their customers’ identities and assess any risks that come with the relationship.

The Bank of Algeria and the Financial Intelligence Processing Unit (CTRF) oversee these rules, ensuring compliance across financial institutions and businesses. If your business is operating here, you’ll need to adopt processes to confirm your customers’ identities using government-issued documents. This includes keeping track of any changes in customer information and flagging unusual transactions.

If you’re already familiar with international KYC practices and Financial Action Task Force (FATF) standards, this should feel pretty familiar.

KYC Requirements in Algeria: What Companies Must Do

The Loi n°05-01, enacted on February 6, 2005, addresses Algeria’s commitment to preventing money laundering and financing terrorism.

This law, later amended by Ordinance n°12-02 in 2012, outlines strict measures for financial institutions and other regulated entities. It empowers Algerian authorities to take proactive actions, such as freezing assets and imposing penalties on non-compliant entities.

Below, we will discuss some of the key provisions laid by law.

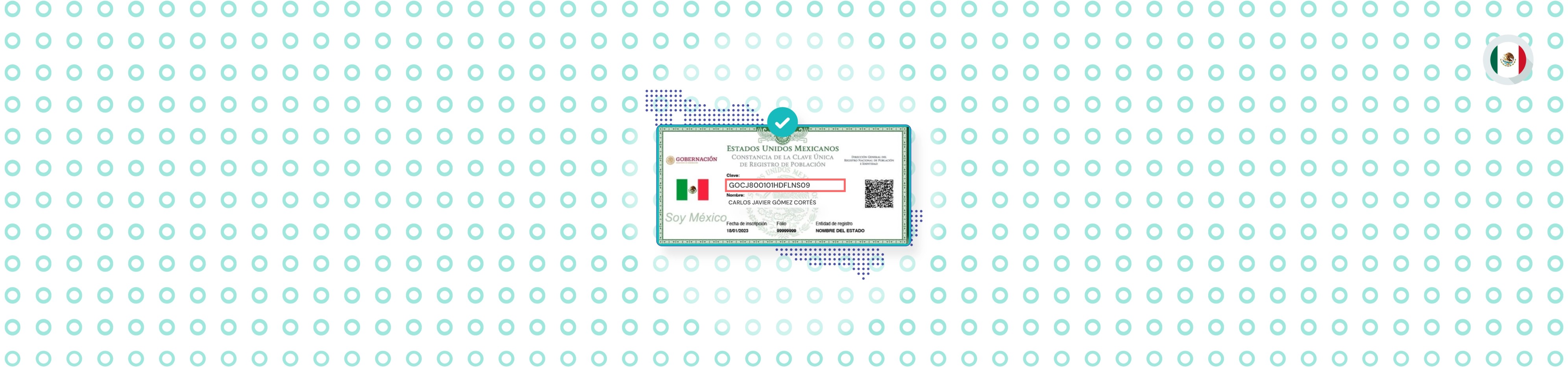

1. Verify Identity Using Official Documents

Companies must rely on official documents. Algeria’s KYC document requirements for identity verification include:

- Algerian National Identity Card

- Passport

- Driver’s license

These documents must be validated for authenticity, ensuring that all security features are intact, such as holograms, expiration dates, and valid photo identification

2. Proof of Address Documentation

Algerian law mandates that businesses also verify the customer’s address. Acceptable proof includes recent utility bills (e.g., gas, electricity), a bank statement showing the customer’s name and address, or an official document from a government agency

3. Ongoing Monitoring of Transactions

Businesses are required to monitor customer transactions continuously, especially when dealing with larger sums or unusual activity. This involves flagging any transactions that don’t align with a customer’s typical financial behavior

4. Record Retention

All records related to customer identities, transactions, and due diligence must be kept for a minimum of five years after the closure of accounts or the completion of a business relationship. This ensures that businesses can provide the necessary documentation for audits or investigations into potentially illegal activities

5. Compliance with AML Guidelines

Companies are also required to collect and retain information about the origin of funds during customer onboarding, particularly if the customer is involved in high-risk transactions or is politically exposed.

Automating KYC in Algeria

In Algeria, manually verifying customers can be slow and prone to mistakes. And with the regulatory landscape here, that’s a risk you don’t want to take. Thankfully, you can automate things to stay on top of things in real time, so you’re always compliant without breaking a sweat.

With a solution like Signzy’s KYC API, you can streamline the entire process. It allows you to verify identities quickly, monitor transactions efficiently, and store all required data securely. As a result, you can focus on growing your business without worrying about constantly keeping up with complex regulations.

See how Signzy’s automation ensures full compliance. For any query, contact us now.

Now, finally, let’s see the KYC/AML framework you can build to maintain compliance across North African regions.

FAQs

Do foreign companies need to follow Algerian KYC regulations?

Yes, foreign companies doing business in Algeria or engaging in transactions involving Algerian customers must comply with local KYC regulations.

How does automation help with KYC compliance in Algeria?

Automation speeds up the process, reducing errors and ensuring real-time verification and monitoring. It also helps businesses stay compliant with minimal manual intervention.

What happens if a business fails to comply with KYC in Algeria?

Failure to comply with KYC regulations can result in heavy penalties, including fines and potential legal action, as well as reputational damage.

Can third-party services be used for KYC compliance in Algeria?

Yes, businesses can use third-party services for KYC compliance, but they remain responsible for ensuring the third party meets Algerian regulatory standards.